As the stock market heads into the last day of the month a lower weekly close is a real possibility but instead we closed mixed. The Spyder Trust (SPY) has recorded strong gains over the previous four weeks. A lower week close would not change the intermediate term outlook but would be consistent with the recent shift in sentiment.

In the latest AAII survey the bullish % dropped 4.2% to $31.3% as it appears they are becoming more skeptical about the market's rally. Over 40% are still neutral on the outlook for stocks while 28.4% are bearish. There does seem to be more of a shift to the bullish camp by the financial press and media as they are belatedly jumping on the bullish bandwagon.

In my April 25th column " A Bull in Sheep's Clothing?" I made the case why "the current market is a "Bull in Sheep's Clothing" as the market's underlying strength is being camouflaged. The strong action of the Advance /Decline lines (see market Wrap Section) is a clear sign of the market's underlying strength and the low level of investor participation it is a strong indication that a new high in the averages will not coincide with a major bull market top."

At the time most on Wall Street did not believe in the rally from the February lows and some felt we were in a bear market. I pointed out that historically real bull market tops generally coincide with a high level of optimism and bullishness. That is certainly not the case now and in April I thought that if "we do see new highs I would expect to see a surge in articles that argue that the bull market is over."

The new highs in the S&P 500 and the major advance/decline lines has helped to uncover the bull market but it will likely another strong rally phase before the bullish camp will get crowded enough to set the stage for a more severe correction.

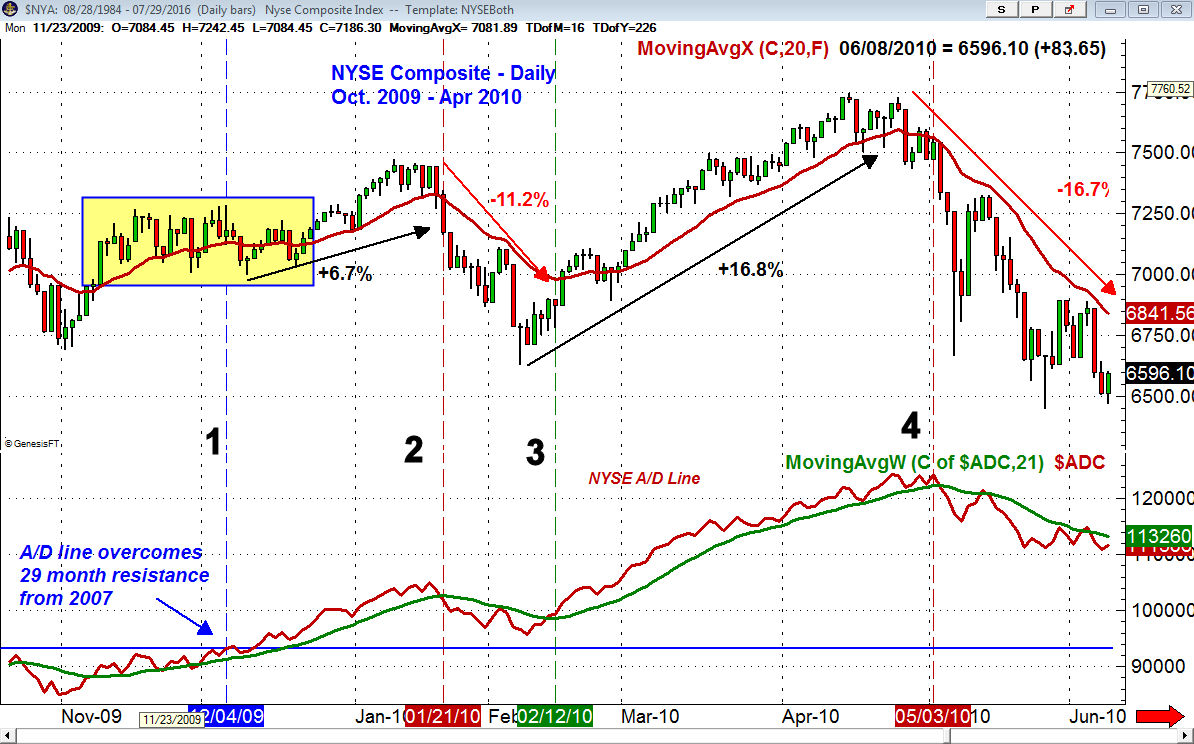

My analysis last week focused on previous instances where the NYSE A/D line had broken out of long-term trading ranges. It supported my view that in the months ahead stocks are likely to be much higher. It also illustrated that there are likely to be bumps along the way which will keep many nervous investors from becoming too bullish.

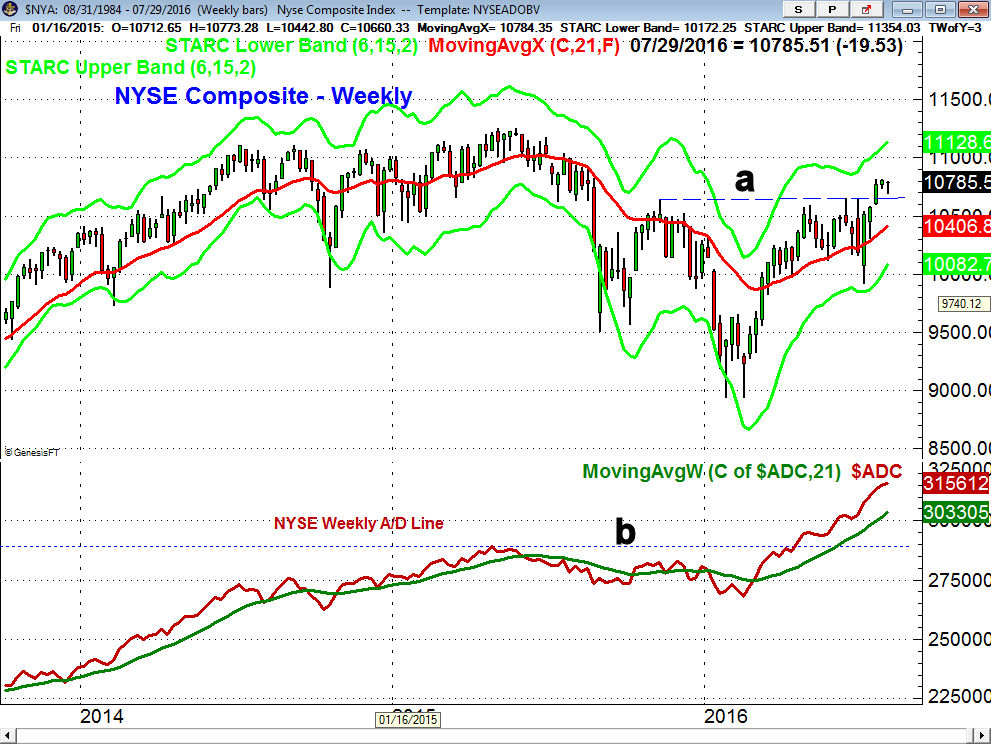

In December 2009 (line 1) the NYSE A/D line overcame twenty-nine month resistance and of course the major averages have been making new highs ever since. This resistance was even more pronounced that the eleven month resistance that was overcome in April 2016. The daily chart of the NYSE Composite allows one to more closely analyze what happened in 2009.

The NYSE Composite stayed in a range after the breakout before beginning a 6.7% rally that lasted until January 21st when the A/D line dropped back below its WMA (line 2). This negative signal was followed by an 11.7% correction that lasted just three weeks in a correction. The decline was spurred over concerns that debt problems in Greece could spread to Spain and Portugal.

Five days after the low, on February 12th (line 3), the A/D line turned positive. Over the next ten weeks the NYSE Composite gained 16.8% as Euro zone fears dissipated. The drop in the NYSE A/D line below its WMA on May 3rd (line 4) was the start of a 16.7% drop that took prices lower into June. The SPY still was able to record a 15.5% gain in 2010.

So what might this mean for 2016? As I discuss in the market Wrap Section the current sideway pattern in my view will be resolved by another push to the upside. The initial targets are in the $220 area but the length of the sideways pattern makes a rally to the $224-$226 area possible. Such a rally is likely to be followed by a correction that is sharp enough to dampen down the bullish sentiment. I would not expect to see double digit correction like what occurred in 2010.

As the overall market has moved sideways for the past twelve days I have avoided adding to longs in the market tracking ETFs that were bought near the early July lows. This is because the stop on SPY or IWM would need to be 5% or more under the entry level. Also the original positions already had nice gains and the next targets were only 2-3% higher.

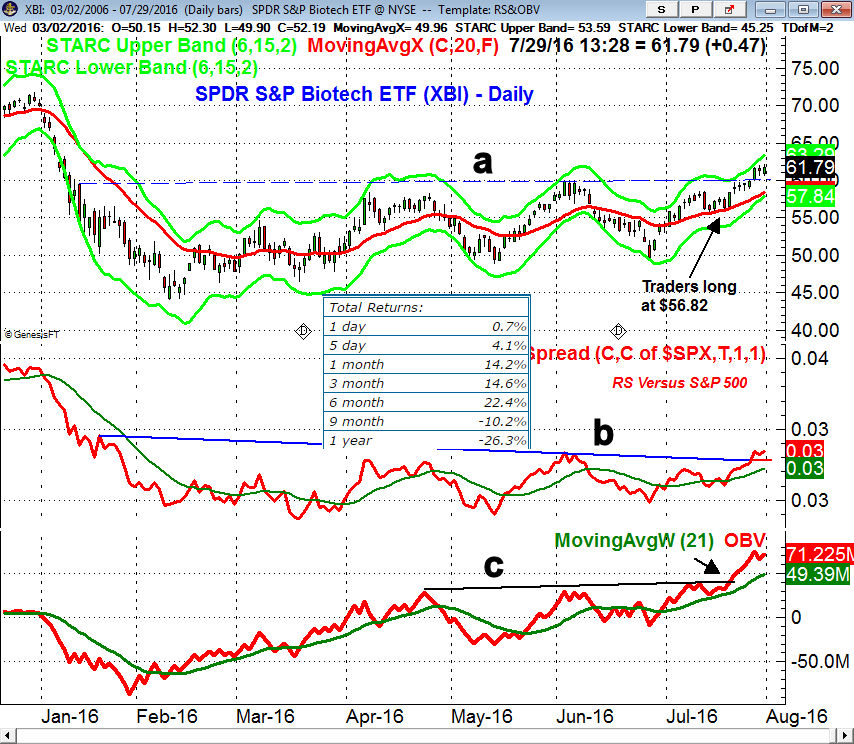

That has not been the case with some of the other ETFs as there has been quite a bit of sector rotation as some ETFs that had been lagging the market are now coming to life. The SPDR S&P Biotech ETF (XBI) was recommended to Viper ETF traders on July 18th and this week it has closed above major resistance at line a.

This completes the 2016 bottom formation and has initial upside targets in the $68-$70 area. The daily relative performance has confirmed the price action by moving above the resistance at line b. The daily OBV broke through resistance, line c, over ten days ago and volume was strong as prices broke out to the upside.

The inserted performance table on the chart shows that XBI has just been getting stronger. It is up 4.1% in the past five days and 14.2% in the past month but it is down 26.3% for the past year. This performance pattern is typical of what you would see from a new market leader.

It has been much easier for stocks traders as while the major averages are well above the lows from early in the month there are many stocks that are much closer to important support. Linear Technology (LLTC) was featured in an article last week "Focus On Your Entry As Lightning Could Strike" where I stressed the importance of taking the time to fine tune your entry level.

It had presented a classic buy the pullback trade setup for Viper Hot Stocks subscribers. It did correct as expected to below $48 and looked ready for a good 10-15% swing trade. Instead it surged 24% on a buyout offer at $60 per share.

It was a wild week for earnings but the large tech companies reported much better than estimated and it does look like the season will be much better than expected. Our longs stocks overall did quite well after earnings but not Check Point Software (CHKP) as longs were stopped out for a 3.7% loss . The long positions in QUALCOMM (QCOM) and Facebook (FB) made up for the loss as both benefited from their strong earnings reports.

It is not a time to be complacent with your portfolio with the market at all time highs. I urge all of you to examine the stocks, ETFs and mutual funds that your own to see if any changes need to be made. Many years ago I wrote an article "Learn to Drive Your Own 401K" where I explained how you could use the relative performance analysis available for free in stockcharts.com to find out whether your holdings were market leaders or laggards.

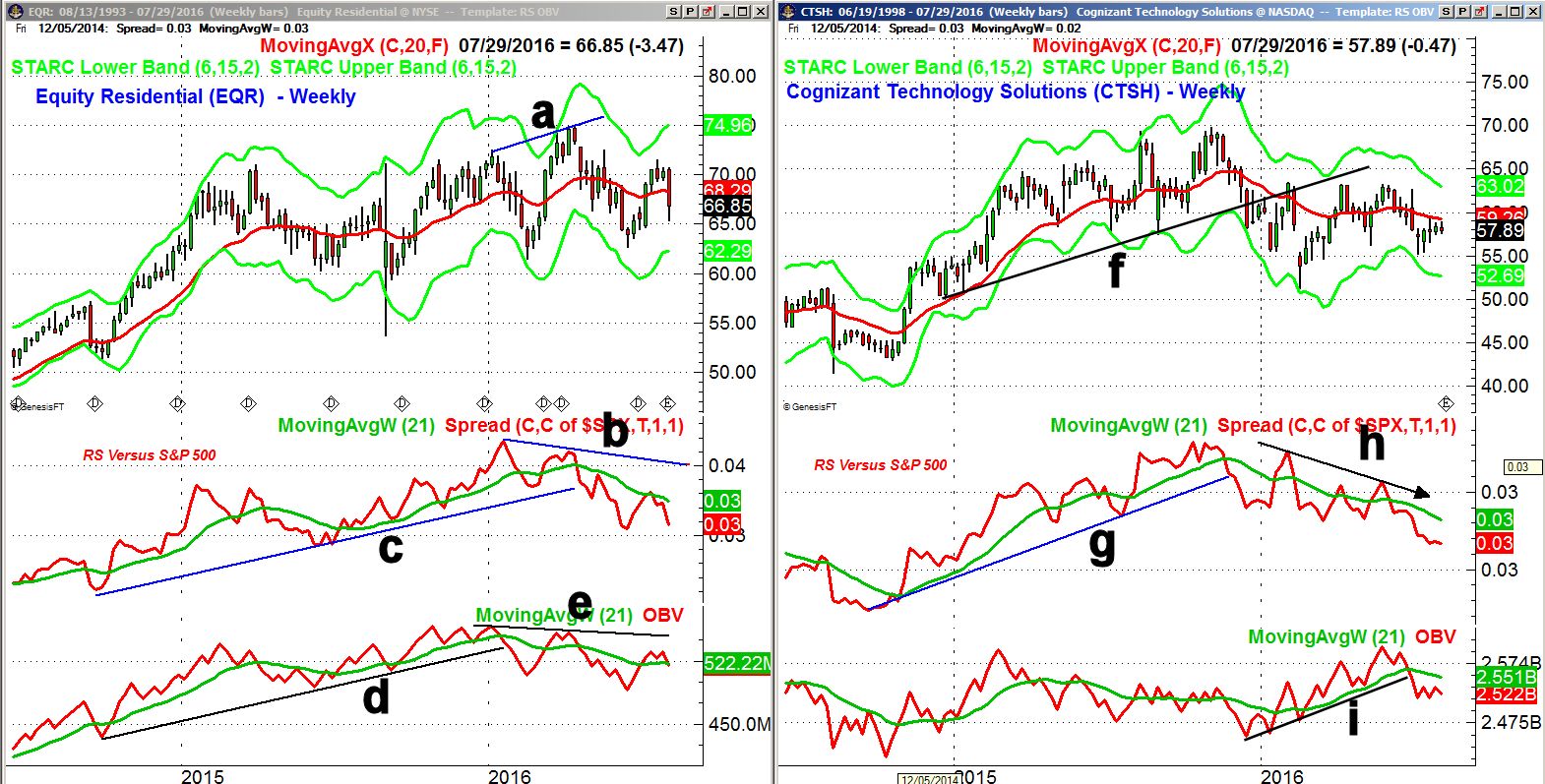

I place quite a bit of emphasis on the relative performance when I analyze portfolios for a clients as part of my mentoring service. Equity Residential (EQR) is stock that came up in one of my portfolio reviews and it was rejected despite its high yield.

As EQR was making higher highs in early 2016 (line a) the relative performance was forming lower highs, line b. This bearish divergence indicated it was no longer a market leader and this was confirmed when the RS line broke its uptrend. A similar divergence was evident in the on-balance-volume (OBV), line e, which was formed after it violated the support at line d.

Cognizant Technology Solutions (CTSH) is down over 3% in the past three months and was another stock that I felt was not a good portfolio holding. The yearlong uptrend, line f, was broken early in the year which was a sign of weakness. The relative performance dropped below its support, line g, at the same time. The RS is now in a well-established downtrend, line h, consistent with a market laggard. The OBV has also recently broken support.

I hope you will take the time to review your portfolio while the market is strong and not wait until it is in the corrective mode. This is important because stocks that are lagging the market when it is moving higher will often drop more when the market declines. If we can help you with this process, you can reach me our or staff at wentworthresearch@gmail.com.

Even though the US market looks clearly positive this is not the case with many of the global equity markets. The German DAX Index had a strong close last week and is now closer to the downtrend, line a, in the 10,500 area. The longer-term chart still looks positive but a break of the downtrend is needed to suggest that the downtrend from the 2015 highs is over.

Japan's Nikkei 225 is still clearly in its weekly downtrend as many are looking for more stimulus from the BOJ in order to push the Yen lower. It did stage a major upside breakout in 2014 so the current pullback still looks to be a correction in the major trend. The next resistance is in the 17,500-750 area with the downtrend in the 18,000 area.

For both of these averages it would be more negative if these indices rally to stronger resistance and then fail

The Economy

The Dallas Fed Manufacturing Survey was negative last month but did show significant. Home prices were down slightly according to the S&P Case-Shiller HPI so the next few months will be important. New Home Sales last week were up sharply as they came in 20K above expectations. In contrast, Pending Home Sales on Wednesday came in lower than expected.

Consumer Confidence was a good 97.3 showing little change from the previous month while the month end reading on Consumer Sentiment was unchanged from the mid-month reading and was down over 4 points.

The Richmond Fed Manufacturing Index improved sharply in July to +10 as it was expected to come in at -10. These numbers can be quite volatile so the next month or two will be important. The Kansas City Fed Manufacturing Index did reverse in July as it dropped back into negative territory.

Durable Goods on the other hand were weaker than expected for the second month in a row - clearly the data is mixed. Finally on Friday, to confuse the outlook even more, the Chicago PMI came in at a strong 55.8 which indicates healthy business activity.

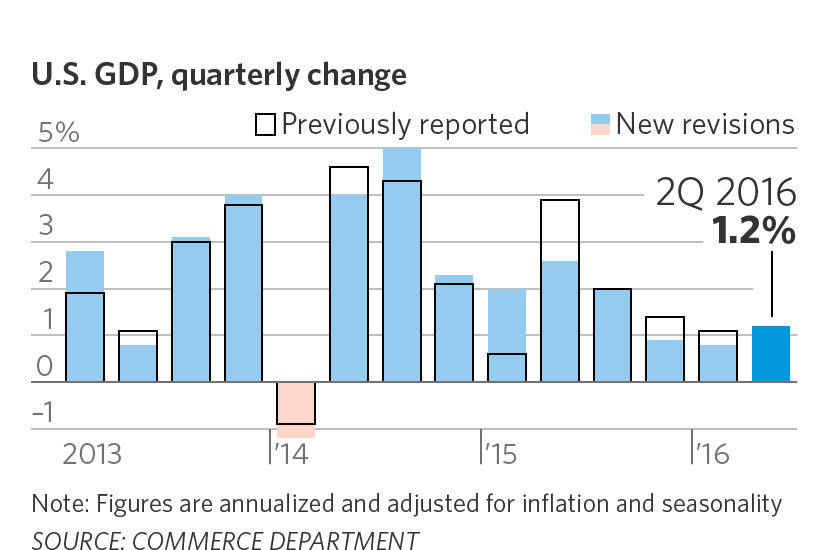

Friday's GDP was also disappointing as it came in at 1.2% which was quite a ways below the consensus estimate of 2.6%. Inside the numbers was a strong 4.2% increase in consumer spending. On the negative side was the sharp drop in inventories which dropped the GDP down by 1.2%.

In addition to Friday's job report we have the PMI and ISM Manufacturing data along with Construction Spending on Monday. The ADP Employment Report is out on Wednesday as is the ISM Non-Manufacturing report which is followed on Thursday by the jobless claims and Factory Orders.

Interest Rates & Commodities

The yield on the 10 Year T-Note dropped last week to close at 1.458% after reaching 1.600% two weeks ago. This indicates the downtrend in yields may have resumed as it closed back below the declining 20 week EMA. Another new low in yields would be a good opportunity to take some profits out of the bond market.

It was another rough week for crude oil as it dropped over $1 on the week but did rally on Friday to close well off the lows.. The sentiment is clearly turning more negative and this was confirmed by the latest COT report which revealed that money managers added 38,000 new contracts on the short side.

The gold futures rebounded sharply last week after the FOMC announcements hinted at a potential rate hike in September. The weekly chart shows that the support from the early 2015 highs, line a, has been tested in the past two weeks. The weekly uptrend, line b, is much lower at $1275.

The weekly OBV broke its downtrend, line c, in early July and has now turned up from its WMA. This is a potential bullish sign. The HPI did form a bearish divergence at the highs four weeks ago, line d, but is now trying to turn up from its WMA. It may be ready to stage an upside breakout. The daily studies are very close now to new buy signals.

The recent action suggests that we may not see the deeper correction I have been looking for and I will be recommending that Viper ETF traders now look to the long side.

Market Wrap

Only the Nasdaq Composite, mid-cap S&P 400 and small cap S&P 600 managed gains last week with the Nasdaq leading the way up 1.2%. The Dow Transports lost 1.5% followed by a 1.3% drop in the Dow Utilities. The Dow Industrials were down 0.80% and the S&P 500 managed a slight gain. The weekly A/D numbers were positive.

For the month the Dow Industrials were up 2.8% while the S&P 500 gained 3.6%. The small cap Russell 2000 was up a powerful 5.8% for the month and the Nasdaq 100 gained over 7% as they took over leader ship in the past two weeks.

The resurgence of the big tech stocks powered the technology sector to a 2% gain last week swamping the 0.5% gain in health care. Any bullish sentiment from July's performance may be dampened by the historically dismal performance of stocks in August which has averaged a 1.3% loss in the past two decades.

The weekly chart of the NYSE Composite shows the breakout above resistance, line a, three weeks ago. The weekly starc+ band is at 11,128 with the 2015 high at 11,254. The weekly NYSE A/D line made another new high and still looks strong though the gap with its WMA has become even larger. The pullback last week brought prices close to the 20-day EMA at 10,677. The daily starc- band is now at 10,622.

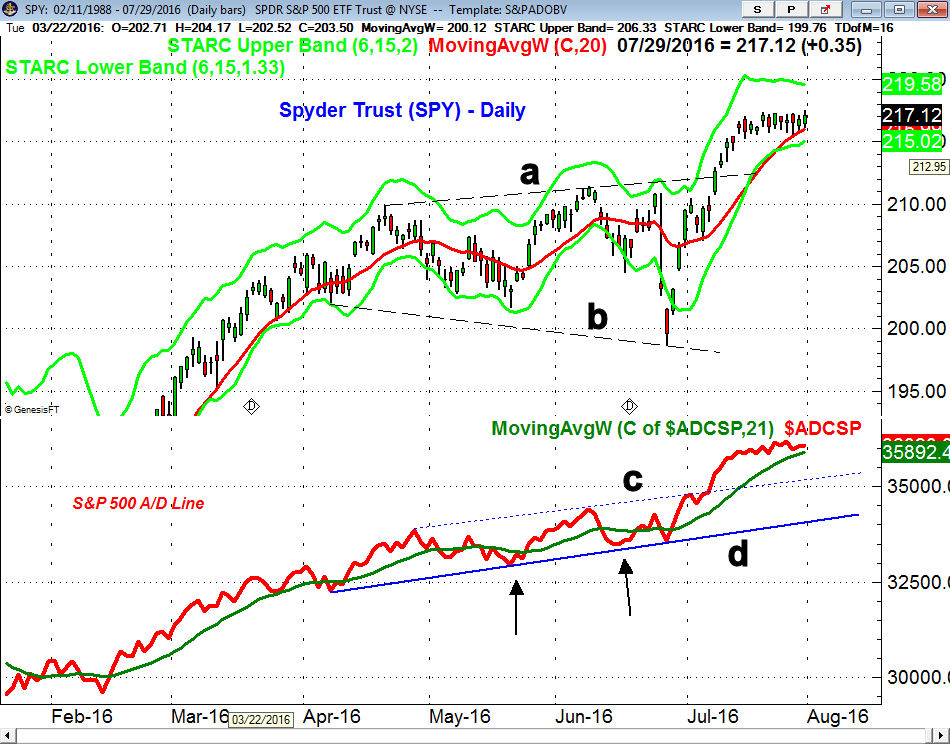

The Spyder Trust (SPY) made a marginal new twelve-day high on Friday and did manage to close higher on the day. The 20-day EMA at $215.99 is now being tested with the monthly pivot at $213.91. The next upside target is in the $219-$220 area but there is the potential for a run to the $222-$224 area.

The sideways action in the S$P 500 A/D has brought it closer to its WMA but a 1-2 day drop below its will not necessarily signal a deeper correction. There is further support for the A/D line at line c, which was the breakout level. It would take a drop below the support at line d, and the May-June lows (see arrows) to turn the intermediate term trend negative.

The iShares Russell 2000 (IWM) has near term support in the $118-$120 area with monthly pivot support at $115. There is monthly pivot resistance now at $124.45 with additional targets in the $126 area. Volume expanded Friday which is a short-term positive.

The PowerShares QQQ Trust (QQQ) has monthly pivot and 20 day EMA support in the $112.50 area. The weekly starc+ band is now at $116.33 with monthly pivot resistance at $118.32. The A/D line has confirmed the new highs and is well above its WMA.

What to do? The tech earnings last week caught many by surprise but the very negative sentiment in May had me looking for earnings to get better not worse. The economic data is still lackluster but the internal numbers indicate the GDP was not as bad as the headline number indicated. It will be important that there is further improvement in the manufacturing data as we head into the fall months.

A sharper correction over the short term cannot be ruled out. The QQQ and IWM are further above support and are a bit more extended. The SPY is likely closer to a short-term low. I do expect the stock market to resume its uptrend in the next few weeks but I will be watching the market closely for signs that it is losing upside momentum.

The next rally is likely to be accompanied by an increase in bullish sentiment and it is likely to be followed by a more meaningful correction. Such a decline should provide a good opportunity for investors to add to their long positions.

For investors and traders you might consider the Viper ETF Report were I give specific buy and sell advice on both market tracking and sector ETFs

If you are a stock trader I typically make 1-3 new recommendations each week in the Viper Hot Stocks Report. Each service is updated twice a week and is only $34.99 each per month. The subscription can be cancelled on line at any time.

Comments

comments