September 17th 2024

The focus last week was on the latest data on inflation from the Consumer Price Index and the markets focused on the fact that the “increase in overall inflation slowed to 2.5% from 2.9% and hit the lowest levels since 2021.”

The price action in the S&P 500 reflected an important change in the market outlook as it declined for the first 90 minutes to a low of $539.96. That was a 1.6% decline from Tuesday’s close. The S&P rallied from the lows to close at $554.36, a gain of.2.6% for the day. The Invesco QQQ Trust (QQQ) was also down sharply early in the day and then closed with a 2.2% gain for the day.

For the week the gains were even more impressive as the Spyder Trust (SPY) was up 4% and the QQQ rose 6%. For the week on the NYSE Composite, there were four times more advancing than declining stocks.

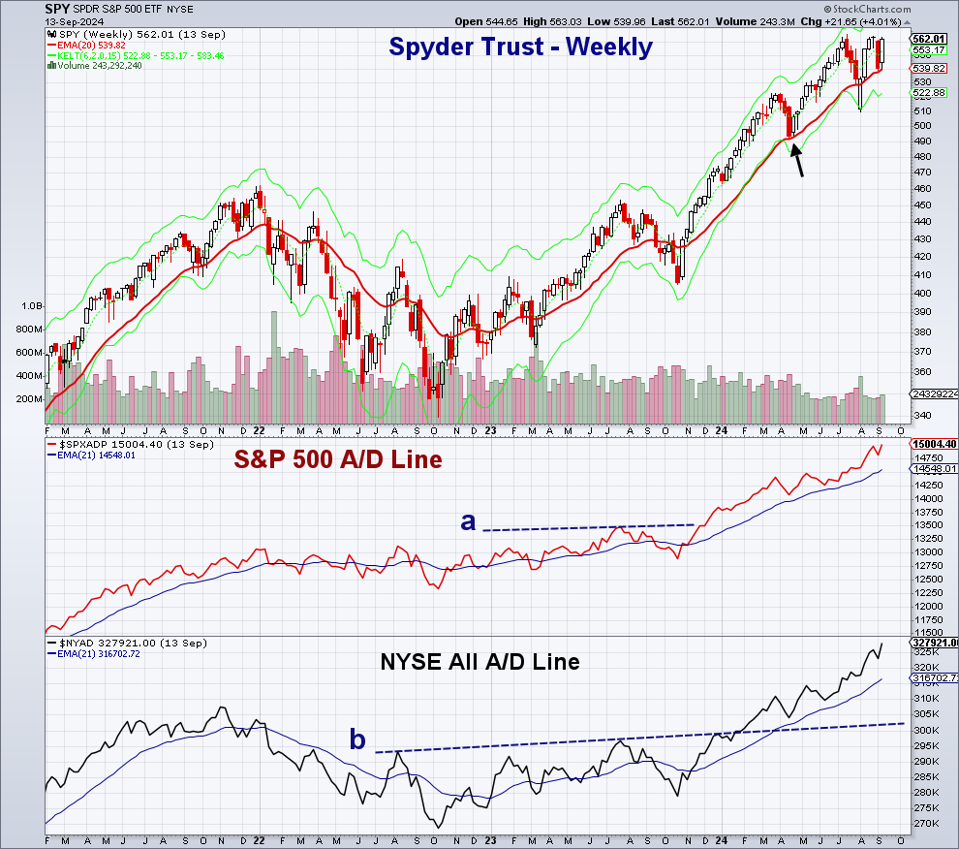

The weekly chart of the Spyder Trust (SPY) shows that it tested the rising 20-week EMA at $541.91 last week before closing strong. I have often found that this weekly EMA to often be a reliable level of support when it is rising strongly as it was at the April correction lows (see arrow). In August SPY dropped well below the EMA but then closed the week back above the EMA.

The positive price action is confirmed by the market internals as the weekly S&P 500 Advance/Decline Line made a new high last week. It is leading prices and does project a new high for the SPY with the weekly starc+ band at $584.80. The A/D line rose above key resistance, line a, in December 2023 which was a major bullish development

The NYSE All A/D line that tracks all instruments on the NYSE Composite also made a new high last week as it rose sharply. This A/D line moved through resistance, line b, early in 2024 and has stayed above the strongly rising EMA all year. The NYSE Stocks Only A./D Line is rising strongly but has not yet made a new high.

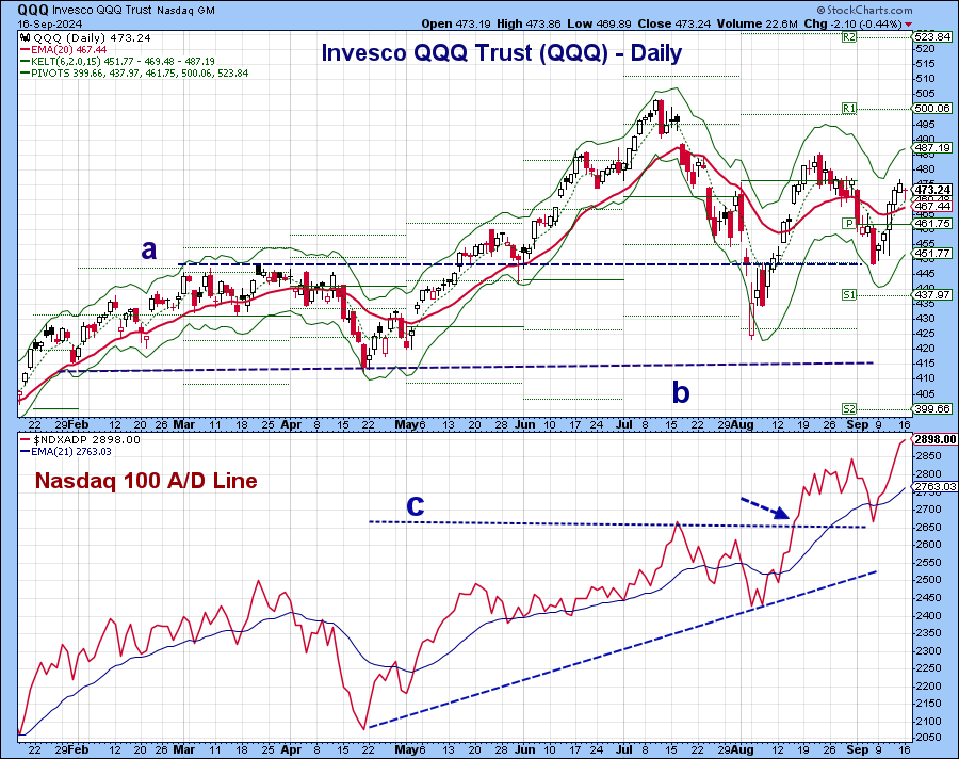

The Invesco QQQ Trust (QQQ) has been out of favor since it peaked in July at $503.52 as it then dropped below its weekly starc- band in early August (see arrow) with a low of $423.51. The strong close last week at $475.34 was not enough to convince many that QQQ still had upside potential. On a move above the August high at $485.54 the weekly starc+ band is at $509.60 with chart resistance, line a, at $522.81. There is support at the two-week low of $448.19.

The weekly Nasdaq 100 A/D line reveals a much more positive outlook than the chart as it moved above resistance, line b, just one week after the August low (point 1). The A/D line made a new high last week that projects a new high in the QQQ. This was the case for the S&P 500 in June 2023. For the weekly A/D line analysis to turn negative it would have to drop below its WMA and the August lows.

The weekly relative performance (RS) rose last week after reaching support at line c. It now needs to move above its WMA to signal that QQQ is again leading the S&P 500. Even though the major averages were higher on Friday there was a slight loss of upside momentum and this turned my focus on Monday’s trading.

In Monday’s trading, the Dow Industrials were up 228 points to close at a new high while the S&P futures were just barely higher but the Nasdaq Composite as well as the Nasdaq 100 were down almost 0.50%. More importantly on the NYSE, there were 1987 advancing stocks with just 814 declining stocks. The Nasdaq A/D numbers were also positive.

There is daily chart support for the QQQ at $467.55 with the monthly pivot at $461.75. Once above last Friday’s high at $476.53, then the August high at $485.54 is the next barrier on the upside. The monthly R1 resistance is at $500.06 with the R2 at $523.84.

The QQQ decline in early September increased the negative sentiment but the Nasdaq 100 A/D line just retested the breakout level at line c, before reversing to the upside. The A/D line moved to a new high last Thursday and was a bit higher on Monday.

This is a bullish setup leading into the FOMC meeting and the expected rate cut announcement on Wednesday. While the A/D line could drop back to its rising EMA but only a drop below the early September lows would turn the analysis negative.

I also often look at fundamental data from a technical perspective. Over the past year the negative public view of the US economy to many has been in contrast to the strong economic data that many of us have observed.

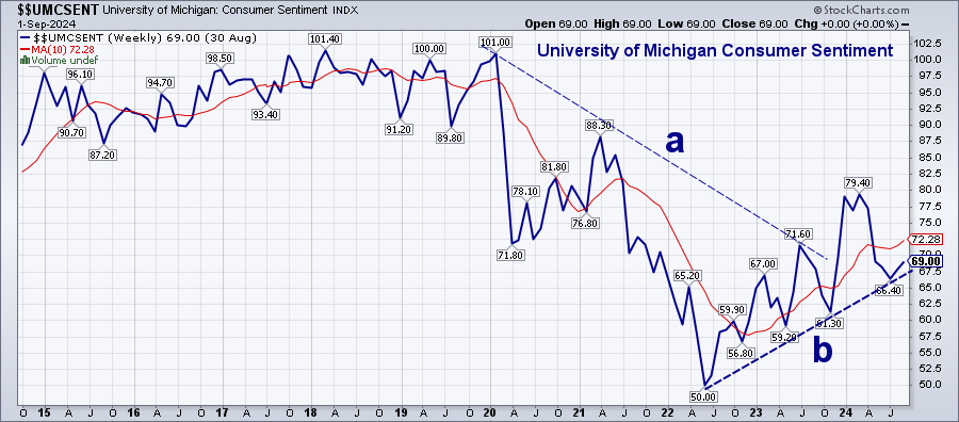

The University of Michigan Consumer Sentiment reports their readings from their surveys twice each month. It peaked at 75.40 in early 2024 and then dropped to a low of 66.40 in July. This was during a period when inflation seemed to be declining, employment was strong as were corporate earnings, and GDP forecasts.

Consumer Sentiment had been in an uptrend since the 2022 low of 50 as the downtrend, line a, was broken in late 2023. In last week’s mid-month reading, the sentiment rose to 69, after testing the uptrend, line b. I expect these numbers to improve further as both mortgage rates and crude oil prices continue to move lower. This is likely to translate into increased consumer spending.

Another strong market rally may again be led by the growth stocks which were also out of favor in early 2023 and 2024 but turned out to be the leaders. Many reasons including the uninverted yield curve recessionary fears, too expensive stocks, and negative earning forecasts are likely to be used as arguments against investing in stocks.

Those sectors that look to best to me are the Communication Services Sector (XLCCommunication Services Select Sector SPDR Fund) which is already close to an upside breakout. I also like Heath Care Select Services (XLVHealth Care Select Sector SPDR Fund) and Financial Select Sector (XLFFinancial Select Sector SPDR Fund). Stay tuned for regular updates as I just finished a long-overdue overseas vacation.