The stock market was able to rally last week despite the larger-than-expected 0.50% rate cut by the FOMC. As is often the case the averages gyrated after Fed Chair Powell's press conference and higher open the Dow Industrials closed down 293 points.

Most will be happy that September is now over as the stock market had a rough start for the month as on September 3rd the S&P 500 gapped 25 points lower and closed down 2.1% while the Nasdaq Composite was down 3.1%. Nvidia Corp (NVDA) was down 9.5%.

The selling accelerated for the next three days dropping to a low of 5402.62 which was a decline of 4.3% from the pre-labor day weekend close of 5649, point a. In my view, the drop was due in part to the widespread stock market commentary warning investors and traders of September’s poor seasonal track record.

Therefore many were on the sidelines or short when the S&P reversed to the upside on September 11th, point b, in reaction to the CPI report. This I felt “ reflected an important change in the market outlook.” The bullish action of the advance/decline lines set the stage for the upside breakout in the S&P 500 in reaction to the FOMC announcement.

My view of investing or trading based on seasonal tendencies was reiterated in 2015. “I have written many times in the past about seasonal tendencies and I have always stressed that one should only invest or trade a seasonal trend when the technical studies are in agreement.”

Some investors and traders fail to recognize that comments like “the worst performance of any month” are mostly based on averages. In this case, going back to 1945. The unanimity of the commentary I think led to an oversized short position heading into September.

Many who took a bearish bet would be surprised to learn that since 2006 the S&P 500 has had September gains of 2.46%, 3.58%, 3.68% and even up 8.71% in 2010. In fact, over the past seventeen years, it has been higher nine times. Exposure to this data may have kept some from selling their positions or buying puts based on the long-term averages.

The lower close after the FOMC announcement had some prepared for heavier selling the next day. Instead, the overnight trading was very positive as the Spyder Trust (SPY) opened 10 points higher or 100 points higher on the S&P 500. This was likely quite tough for those on the wrong side.

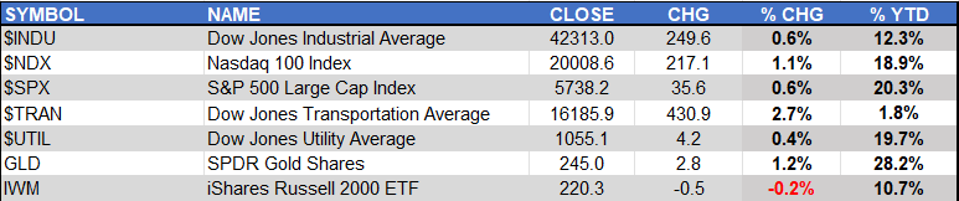

The bullish end to the week moved most of the averages higher led by the Dow Jones Transportation Average which was up 2.7%. It was followed by a 1.2% in the SPDR Gold Trust (GLD) which was up 1.2% just barely stronger than the Nasdaq 100 (NDX) 1.1% gain.

The S&P 500 and Dow Jones Industrial Average were both up 0.6% while the iShares Russell 2000 (IWM) was down 0.2%. For the week on the NYSE, 1672 issues were advancing and just 1190 declined.

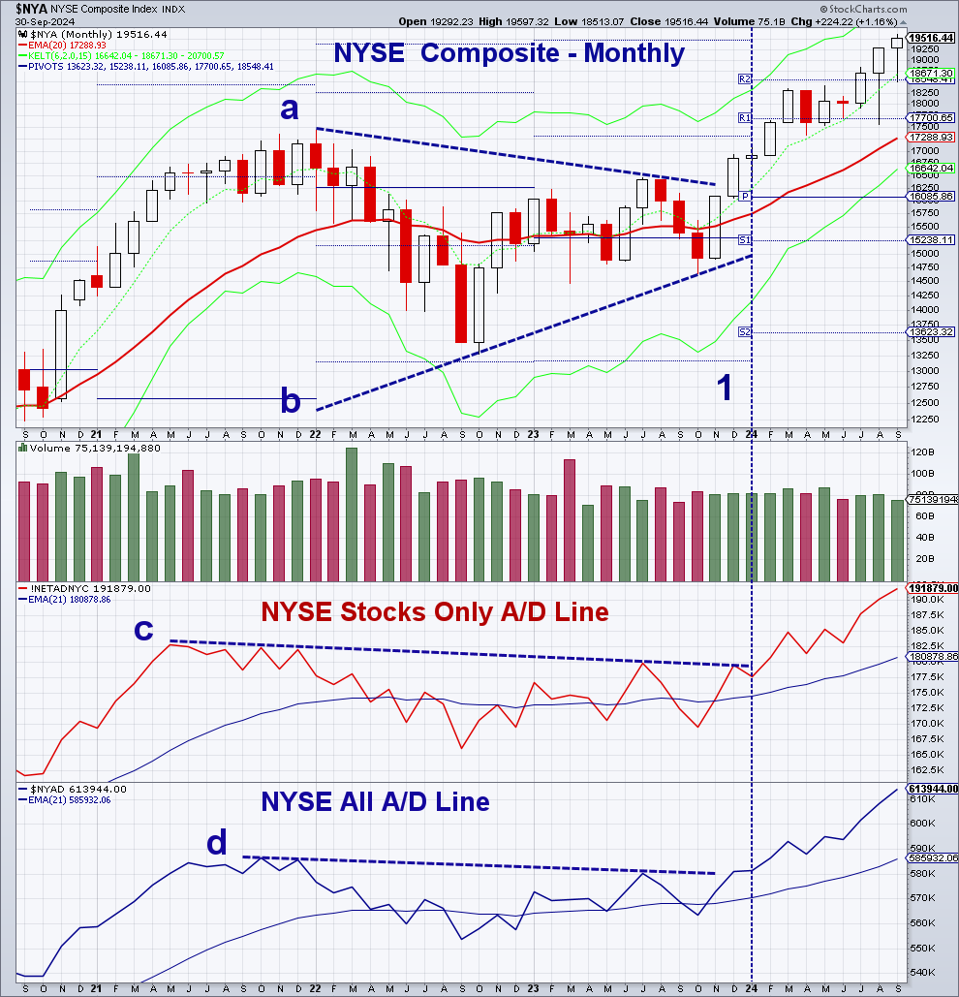

The data is still pointing higher as the monthly chart of the NYSE Composite completed a flag formation, lines a and b, in December of 2023. At the time both the NYSE Stocks Only Advance/Decline line and the NYSE All Advance/Decline were above their EMAs and therefore positive.

In January of 2024, both advance/decline lines moved through their long-term resistance, lines c and d, which confirmed the positive price action. As we move into October both A/D lines are positive as they are well above their rising EMAs. The widening gap does mean they are getting overbought.

In addition to the advance/decline data I also focus on the price and volume data. The price data determines the moving averages and I concentrate on the 20-period exponential moving averages (EMAs) on the monthly, weekly, daily, and even the hourly data.

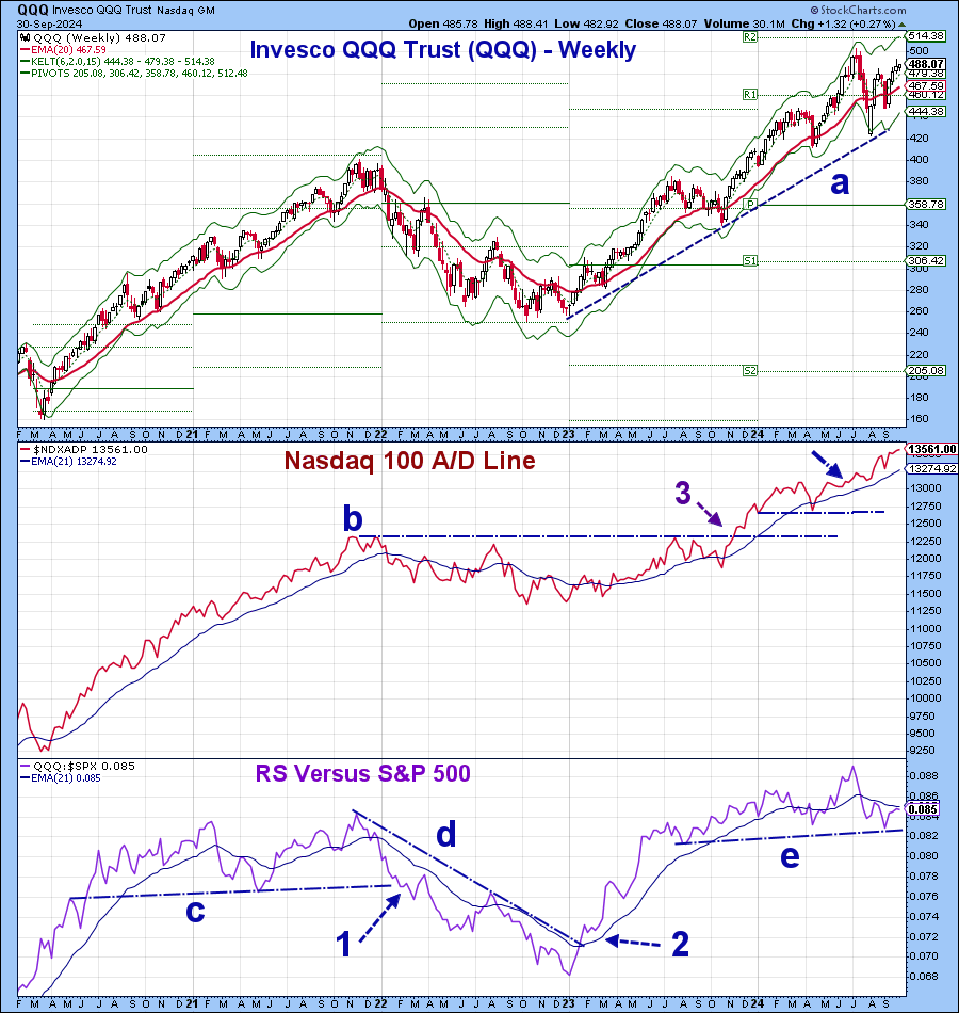

The price data is used to determine the pivot levels as well as the starc bands. This weekly chart of the Invesco QQQInvesco QQQ Trust Trust (QQQ) includes the yearly pivot levels for the past four years. These are based on the prior year's data. From early 2020 until early 2022 QQQ stayed above its pivot. In March 2023, QQQ closed back above the pivot and opened 2024 well above the yearly pivot at $358.78.

The weekly Nasdaq 100 Advance/Decline line broke out above the long-term resistance, line b, in November of 2023 (point 3). It has been forming higher highs and higher lows since then as the decline in April 2024 held support before it again surged higher.

The weekly relative performance (RS) is one of the key tools I use to determine whether SPY or the QQQ is going to be the best performer. The RS peaked in November 2021 and then dropped sharply. The RS support, line c, was broken in early 2022 (point 1) which indicated that QQQ was now lagging not leading the SPY.

The RS downtrend, line d, favored the SPY over the QQQ in 2022. The break of this downtrend and the move above the rising EMA was a sign that QQQ was again leading the SPY.

In 2023 the RS stayed above its EMA but it has crossed above and below it several times in 2024. Currently, the RS is below its EMA but rising. If the RS is now able to move back above its EMA that will be a sign that QQQ is again a market leader.

Given the global risk factors and the upcoming election, I would not be surprised if there is a sharp 1-3% pullback or two in October. But the strong trend in the advance/decline lines is a positive factor for stocks after the election and into the end of the year.

Going forward try to just use hard data in your decision-making process for investing or trading. Avoid making decisions based on any general market commentary, seasonal analysis, or the public investing stance of any large hedge fund. This will help you avoid future bear or bull traps.