June 24, 2017: It was another choppy week for the stock market as after a powerful close on Monday, stocks quickly reversed the following day. For the rest of the week the S&P 500 was under pressure while the tech heavy Nasdaq 100 continued to move higher.

The split market has been confusing investors since the brief tech meltdown almost two weeks ago. I am not surprised that many are already regretting selling in reaction to the Goldman warning about the high flying tech sector. My recent article in Benzinga may help you avoid acting irrationally during the next sharp market decline.

I hope many investors have gotten the message from me over the years to distrust the opinion of the large hedge fund managers and firms like Goldman Sachs. Many may remember last June when Goldman warned prepare for a "major drawdown."

Their tune did not change by August as they were still advising clients to put money into cash as they were neutral on stocks for the next twelve months. The Spyder Trust (SPY) is up 14.3% since August 1, 2016.

There are a number of cynical traders who wonder if these big name firms and managers are trying to gain a quick financial advantage by scaring the market but that is just conjecture. I do know that it is possible to sometimes profit by taking the opposite side. Unaware of the day’s Goldman downgrade I recommended Micron Technology (MU) to Viper Hot Stock traders before it opened lower at $27.56 on May 8th. It has only traded higher since then.

In choppy markets it is especially hard to stick with you plan and to avoid reacting to what you read or hear. My market analysis is based on the market data with the main focus on the advance/decline numbers and the actual price data of the market I am investing or trading.

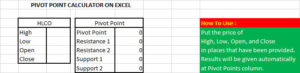

One of the simplest methods I follow is comparing the Friday’s closing price of an ETF or stock to its quarterly pivot which is calculated by looking at the high, low and closing price of the previous quarter. The QPivot is equal to the (H+L+C)/3.

Like any method there are occasional whipsaws but throughout the current bull market it has had many success stories. The QQQ closed on July 1st 2016 at $106.98 (point 1) which was above the 3rd quarter pivot as it reversed the signal from the previous week. It had been above the QPivot since the first week of the 2nd quarter.

This signal stayed in effect until November 4th 2016 it closed at $113.65 (point 2) which was below the 4th quarter pivot at $114.84 (based on the 3rd quarter data). But next week it closed at $115.80 which was back above the quarterly pivot.

The pivot was also tested the week of December 2nd but it ended the week above the QPivot. The first week of 2017 the QQQ closed at $121.35 which was well above the 1st quarter pivot at $117.82.

For the 2nd quarter the low has been $130.03 which was well above the quarterly pivot at $128. Based on data through June 23rd the 3rd Qpivot is tentatively at $138.27.

One of the week’s biggest winners was the Vanguard Health Care ETF (VHT) which was the favored Viper ETF pick over Health Care Sector Select (XLV) as it has 361 holdings versus just 61 for XLV. For those not in VHT longs were subsequently recommended in XLV.

VHT started off the New Year above the 1st QPivot at $126.88 though it was tested in late January. The 2nd QPIVOT at $135.47 was briefly exceeded by a few cents on April 18th as the low was $135.40. It closed the week well above the QPivot and since then the market has not looked back. Viper ETF investors are 100% long VHT at an average price of $135.70 while traders took a 10% profit on 50% of the position last week.

The quarterly pivot can also keep you out of trouble. The SPDR Oil & Gas Exploration (XOP) closed on Friday February 10th at $40.17, point 1, right on the 1st QPivot. The following week it closed at $39.15 and one week later closed at $37.70.

After dropping to $34.40 in late March XOP rallied back to a high of $38.55 on Wednesday April 5th (point 2). This was above the 2nd QPivot but by the end of the week XOP closed at $37.13 indicating that there was no change in trend. Based on data through June 23rd the 3rd QPivot is at $33.15.

So how to get started? Quarterly price data can be found on a number of sites including the Nasdaq.com (link to SPY data). In terms of charts the best I have found so far are on www.freestockcharts.com.

For those who have signed up from my free reports on www.viperreport.com I will be sending out a copy of an excel spreadsheet like the one above that you can use to calculate the quarterly pivot. As part of the signup process you will also be able to download my eBook on trading techniques.

This form will allow you to calculate the quarterly pivots for any ETF or stock you are following. Keep a table so that each week you can compare the final weekly closing price to the QPivot.

Investors should consider waiting for two consecutive weekly closes below the QPivot. Over the past seven years there have been a number of instances when a market tracking ETF has closed below the quarterly pivot for one week but then reversed the next to close back above it.

During panic selloffs a market can drop well below the quarterly pivot during the week but not close the week below it. As part of my premium services I also use the quarterly and monthly pivot numbers (support and resistance) to determine both entry and exit prices.

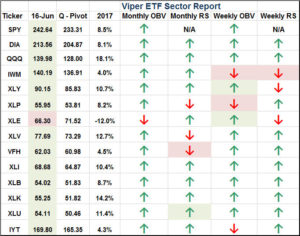

In in each Monday Viper ETF Report I publish this table of the key ETF that includes the QPivot as well as the updated readings of my relative performance and OBV analysis. As of the close on June 16th only XLE was below its QPivot.

The Economy

The economic calendar was light last week though several Fed governors gave their differing views on the likelihood of future rate hikes as some feel low inflation favors a “wait and see” attitude.

Existing Home Sales jumped 1.1% on Wednesday with New Home Sales increasing by 2.9% in Friday’s report. The all-important Leading Indicators rose 0.3% in May and remain in a positive trend. It would take several consecutive lower numbers to send a warning on the economy.

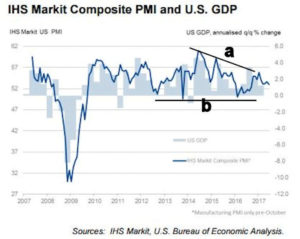

The IHS Market Composite does not look as strong declining last week after testing the downtrend, line a, earlier in the year. A decisive drop below the 50 level for a few months would be a concern.

This week the calendar is full with Durable Goods, Chicago National Activity Index and Dallas Fed Manufacturing Survey on Monday. This is followed by the S&P Corelogic Case-Shiller Housing Price Index, Consumer Confidence and the Richmond Fed Manufacturing Index.

Pending Home Sales are out on Wednesday with the final reading on 1st quarter GDP Thursday. The week ends with the Chicago PMI and Consumer Sentiment.

Interest Rates & Commodities

The yield on the 10 Year T-Note was a bit lower last week as it had the 2nd lowest weekly close of the year. This has kept the weekly as well as the daily downtrend intact. A drop below 2.100% might really get the market’s attention. I am not convinced the low yields are necessarily sending a message about the economy as it may just be nervous investors seeking shelter.

The SPDR Gold Trust (GLD) was barely higher last week but is still above its QPivot at $116.16. The close was right on the flat 20 week EMA. The recent rally failures just above the 61.8% retracement resistance at $121.91 (line a) do not look bullish. The weekly OBV tried to break its downtrend, line b, in April before reversing. The gold mining ETFs have continued to have weekly closes below their QPivots.

Market Wrap

It was another week of sector rotation as the recently hot Dow Utilities lost 1.66% while the Dow Industrials and S&P 500 managed meager gains of 0.05% and 0.21%. The Nasdaq 100 powered by tech and biotech was up 2.2% with the small cap Russell up 0.57%. The NYSE A/D numbers were slightly negative.

Other than health care and tech the other major sectors were lower for the week with the financials closing down more than 1% as they did a bit worse than the industrial sector. Individual investors seem to still be confused as there was little change last week in the AAII survey with 32.7% bullish and 28.9% bearish. The majority (38.2%) are neutral. The CNN Fear & Greed Index is neutral.

The weekly and daily analayis for the Spyder Trust (SPY) remains positive though the ranges have tightened over the past three weeks. The weekly starc+ band is at $248.28 with trading range targets in the $248-$250 area. The 20 day EMA is still rising gradually and is now at $242.11 with more important support in the $240 area. The April high at $238.12 is now more important support.

The weekly A/D line made a new high a week ago and still shows a clear pattern of higher highs and higehr lows. It is well above its WMA and the support at line b. The daily S&P 500 A/D line (not shown) has moved back above its WMA after making a new high on Monday. To signal a deeper correction a day of sharply negative A/D numbers is needed to call the current uptrend into question.

The PowerShares QQQ Trust (QQQ) is still 1.6% below the June 9th high of $143.51. The weekly starc+ band is at $145.87. The Friday close was above the prior week’s doji high of $140.55 so a doji buy signal was triggerred. There is minor support at $139.28 with more important in the $137 area, line a.

The daily Nasdaq 100 A/D line tested its support, line b, last week but then closed the week above its WMA. The weekly A/D line made a new high the week of June 2nd and turned higher last week. The weekly and daily OBV are below their WMAs.

The iShares Russell 2000 (IWM) is still locked in its trading range and needs a close above $142.90 for an upside breakout. Such a move is likely to cause an upward explosion in the overall market. Both the weekly and daily Russell 2000 A/D lines are now above their WMA as the daily flipped back to positive on Friday.

The SPDR Dow Industrials (DIA) made a short term high on Tuesday and pulled back gradually for the rest of the week. The Dow A/D line made a new high on Monday before turning lower but turned up on Friday as it came close to its WMA. The weekly starc+ band is at $217.43.

What to do? It seems like ages since the inauguration as the stock market then broke of its two month post-election range (see Tweet) which was confirmed by the advance/decline lines. Since then investors have been presented with a number of reasons not to buy stocks but the market has continued to move higher.

This has reinforced the merits of not over analyzing the ramifications of the political or global controversies. The positive intermediate term analysis does not warn of a bear market on the horizon yet one cannot be complacent as a 5-10% market correction is a real possibility in the next several months.

As expected last week the technology sector does appear to have completed its correction but another strong weekly close is needed to confirm. Given the gains investors should probably wait for a better risk entry. Health care is also likely to move even higher by year end but it is not a market to chase right now.

The overseas markets, especially Europe, have been correcting despite economic data that continues to improve. This could provide another good buy point this summer. I continually monitor 25 of the largest overseas and country funds in the Viper ETF Report for new opportunities

The Viper Hot Stock portfolio is primarily positioned on the long side right now was there was some buying of tech stocks over the past two weeks. This could change in the coming weeks and I was also fortunate to take some nice profits before the June 9th drop.

If you are interested in specific buy and sell advice, you might consider a one-month investment of just $34.95 for either the Viper ETF or Viper Hot Stocks service. Both services include two in-depth reports per week and subscriptions can be cancelled online at any time.

If you are interested in learning more about my trading strategies, you can download a copy of my eBook and also be added to the list for the free Viper Report emails. Market commentary and technical tips are sent out several time a week.