Given the accelerated selling in the stock market last week and the bear market fever that has been swamping the financial pages since the start of the year more investors seem convinced that a bear market is already underway.

As I noted in The Week Ahead: Can Crude Oil Now Rescue Stocks? the reversal on January 21st was consistent with a short term low as a crude oil rally was expected to be supportive for stocks. A multi-week rally in the Spyder Trust (SPY) to the $195-$198 area is likely needed to set the stage for the creation of a sustainable market bottom. If stocks instead turn lower this week then a drop back to last week's lows or lower before a bottom is complete.

One thing is certain from 120 years of market history, no market goes straight down or straight up. Even though I have stayed off the very crowded bear market bandwagon it is important to understand what a bear market rally looks like so you can recognize one if it occurs.

Therefore I thought I would share an article that was originally posted on June 8, 2008 when I was convinced that we had just completed a bear market rally. I think these examples will give some investors the ability to adjust their portfolio even if it does turn out that we see a bear market rally in 2016. (Helping clients in the analysis and adjusting of their portfolios is one of the services that we provide in our mentoring service.)

There has been much debate among investors and analysts as to whether the rally from the March 17th 2008 lows was the start of a new market uptrend or just a bear market rally. Having experienced, and been fooled by, a number of bear market rallies, I thought analyzing some of the common characteristics might be helpful.

bear1

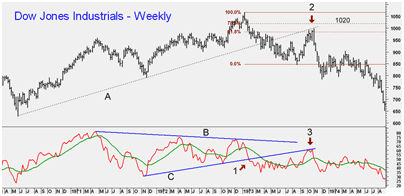

One of the most severe US bear markets occurred during 1973 and 1974 as the Dow Industrials made a high of 1062 on January 11, 1973 and eventually reached a low of 570 in late 1974. One week after the highs, the Dow reversed and closed the week lower. The Dow declined 20% over the next eight months, reaching a low of 845 on August 22.

The weekly chart above covers from April 1970 through August 1974. Below the bar chart is the 14-period Relative Strength Index (RSI) with a 21-period weighted moving average (WMA). The RSI formed a long-term negative divergence between the April 1971 and January 1973 highs, as indicated by line B.

One should remember that the longer it takes the divergence to form, the more important the signal. You will note that at both the 1971 and 1972 highs the RSI dropped below its WMA within a few weeks of the high. Also, at both the 1972 and 1973 highs the weekly RSI additionally formed short-term negative divergence (see circles).

Two weeks after the highs at 1062 the RSI dropped below its WMA, confirming the short-term divergence. The week of February 9th (point 1) the RSI violated key support at line C, while the uptrend in price (dashed line) was not broken until the week of March 23rd.

The rally from the August 22nd lows was quite sharp even though it only lasted ten weeks with the Dow reaching a high of 998 on October 29th (point 2). This was a rally of 18% and, while it slightly exceeded the 61.8% retracement resistance, it did not move above the 78.6% retracement level at 1020. The RSI, on the other hand, just moved up to test its former uptrend, line C, before turning lower. In the next six weeks the Dow dropped 21.4%.

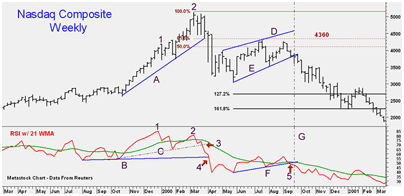

Most of us have not yet forgotten the 2000 bear market in the NASDAQ Composite, which managed to end a few trading careers. The weekly chart shows the March 2000 highs at 5132, and below the bar chart, you will notice that the RSI peaked in January (point 1) and then formed a lower high in March, point 2. The week after the highs, the RSI dropped below its WMA, and the third week after the highs violated its short-term uptrend (line C) as noted at point 3. The violation of longer-term RSI support at line B, point 4, confirmed a significant top had been completed.

The NASDAQ formed a short-term bottom in May with a low of 3042. This was a decline of 40% from the highs. The rebound lasted 3 ½ months but stalled at 4290 just below the 61.8% retracement resistance at 4360. Nevertheless, this was a 40% rally from the lows at 3042. The rebound in the RSI was not nearly as impressive as it just rebounded from a low of 39 back to the 57 area.

The RSI rebound failed and it dropped below its WMA (point 5) one week before the price support, line E, was broken. Using Fibonacci projection analysis, the continuation pattern, lines D and E, gave us the following projections: the 127.2% target was at 2704 and the 161.8% target was at 2252. Both were reached by the end of the year.

The most dramatic bear market of the last 20 years occurred in Japan as the Nikkei (NK225) peaked on December 29, 1989 at 38,950 and reached a low in 2003 of 7603. As you might imagine there were many rallies within this long-term downtrend and many analysts, myself included, were fooled by some of these bear market rallies.

The weekly chart of the NK225 above covers the period from November of 1986 through September 1990. The RSI failed to form any negative divergences at the 1989 high as it made marginal new highs but three weeks after the highs (point 1), it did break significant support (line B). The NK225 rebounded for five weeks before plunging through its uptrend (line A) at point 2. The six-week plunge took the NK225 11,699 points from the highs for a drop of 30%. The ensuing bear market rally lasted nine weeks and took the NK225 back to a high of 33,344 as it stalled at the 50% retracement resistance.

Even though this was a 22.4% rebound from the lows it does not look that impressive on the chart and the RSI was just able to bounce back to the 50 level, point 4. The weekly chart additionally shows a short-term double top that was completed on the break below 31,644 as the selling resumed.

Let's look at this rebound in the NK225 on the daily charts, once again using the 14-period RSI with a 21-period WMA. The RSI formed two short-term positive divergences in March and April (line d), suggesting that a low was being formed. Given the negative readings from the weekly RSI it was expected that any rally would be against the major downtrend. The daily RSI formed its first negative divergence at the June 8th highs (line c) and then violated its uptrend, line d, in late June giving us an early warning signal.

The NK225 rebounded back above the 33,000 level on July 18th but failed to exceed the June highs. The RSI was much weaker on this rally, and on July 20th, the continuation pattern (lines a and b) was completed. The target from the flag formation was in the 27,000 area and was easily met. The 161.8% Fibonacci projection from the April to June rally, as noted on the chart, was at 23,995 where the NK225 stabilized for a month before dropping down to the 20,000 level. The 261.8% projection was in the 18,800 area which was not reached until April 1992.

While I had planned to look at the current market in Part Two of this article, it seems more appropriate to examine the current outlook on the Dow Industrials in Part One as the chart above is through June 6, 2008. The weekly RSI topped in June 2007 and formed the first negative divergence at the July 2007 highs and then was much lower as the Dow made new highs in October (line D). This negative divergence was confirmed the week of November 9th (point 1), when the RSI broke its support (line B).

The weekly RSI stayed below its WMA from October 19, 2007 through March 20, 2008. The Dows rebound from the March lows slightly exceeded the 50% retracement resistance at just under 13,000, but failed below the 61.8% resistance at 13,232. The action in the RSI was classic, as it rebounded back to both the former uptrend (line B) and the bearish divergence resistance at line D (point 3). The RSI has now dropped back below its WMA, but at 43, it is still well above oversold levels.

The daily chart suggests that the rebound from the March lows may be over as the Dow just reached the former uptrend (line A) on May 2nd (point 2). A week later on May 9, the Dow made a marginal new high before reversing and breaking the short-term uptrend, point 3. The daily RSI rebounded to the resistance in the 65-70 area and formed a short-term negative divergence at the May highs (line C).

The RSI has now broken its uptrend and is below its declining WMA. The 127.2% downside projection, calculated from the January lows and May highs, is at 11,250 with the 161.8% projection at 10,700. To validate either of these targets, the Dow needs to break its uptrend at 11,900 (line B) and then close below the 11,630 level which corresponds to the January lows. A close back above 13,140 would reaffirm the uptrend.

On June 22nd, two weeks after this article was released, the Dow Industrials closed below 11,900 and over the next three weeks had dropped 1000 points.

I hope these examples have increased your understanding of bear markets. During the 2007-2008 decline being in the right ETFs or funds helped many portfolios hold up better than the Spyder Trust (SPY). If you want specific entry/exit advice on ETFs you might check out the Viper ETF Report .

1 thought on “Learning From Past Bear Markets”

Comments are closed.