The stock market recorded nice gains on Monday but then returned to its narrow trading range since it has not had a 1% move either up or down for the past month. The Spyder Trust (SPY) has been grinding higher as it is up 1.3% during the period.

Even though the broad market gains have not been impressive the attitude of many professionals, as expected, has become a bit more positive. At the end of February I discussed why investors should not avoid stocks because of their fears over China, weak crude oil prices, earnings or a weak economy.

It was also important that with the close on February 27th "the weekly NYSE A/D line has moved back above its WMA for the first time since the start of the year". The daily chart of the Spyder Trust (SPY) shows the both the bullish divergence at the February lows as well as the break of the downtrend in the A/D line.

Despite the pickup in articles that are more positive on the stock market more high profile bears keep coming out of the woodwork. In a letter to investors in his $28 billion dollar hedge fund manager Paul Singer thinks that the negative yields in many of the world's bond markets has investors facing "the biggest bond bubble in world history" .

He also fears a drop may be very sudden and very sharp. I found it interesting that Elliott further stated "Everyone is in the dark....Experience doesn't count for much, and extreme confidence may be fatal." Is this possibly an excuse for the continued poor performance of the hedge fund industry? It has been my view for over two years that the hedge industry as entered its own bear market. ("The Bubble No One Is Discussing")

In last week's column I wondered why there was not any euphoria amongst stock investors despite the many proclamations of a major bull market top. The bond market is clearly a very crowded trade as nervous investors fight for yields but most bond traders I come across are nervous not euphoric.

These concerns come as the stock market is ready to endure another month or more of obsessive discussion on whether the Fed will raise rates. This Friday Janet Yellen will be giving a widely anticipation presentation that is likely to be fully dissected by the bond market CSIs.

This will be the start of another round of painful debates even though the futures markets currently reflects that there is a low chance of a September rate hike. It seems that many investors are still convinced that a rate hike will be negative for stocks and that it will likely cause a recession. As I have noted in the past this only typically happens late in a rate hiking cycle, not at the start.

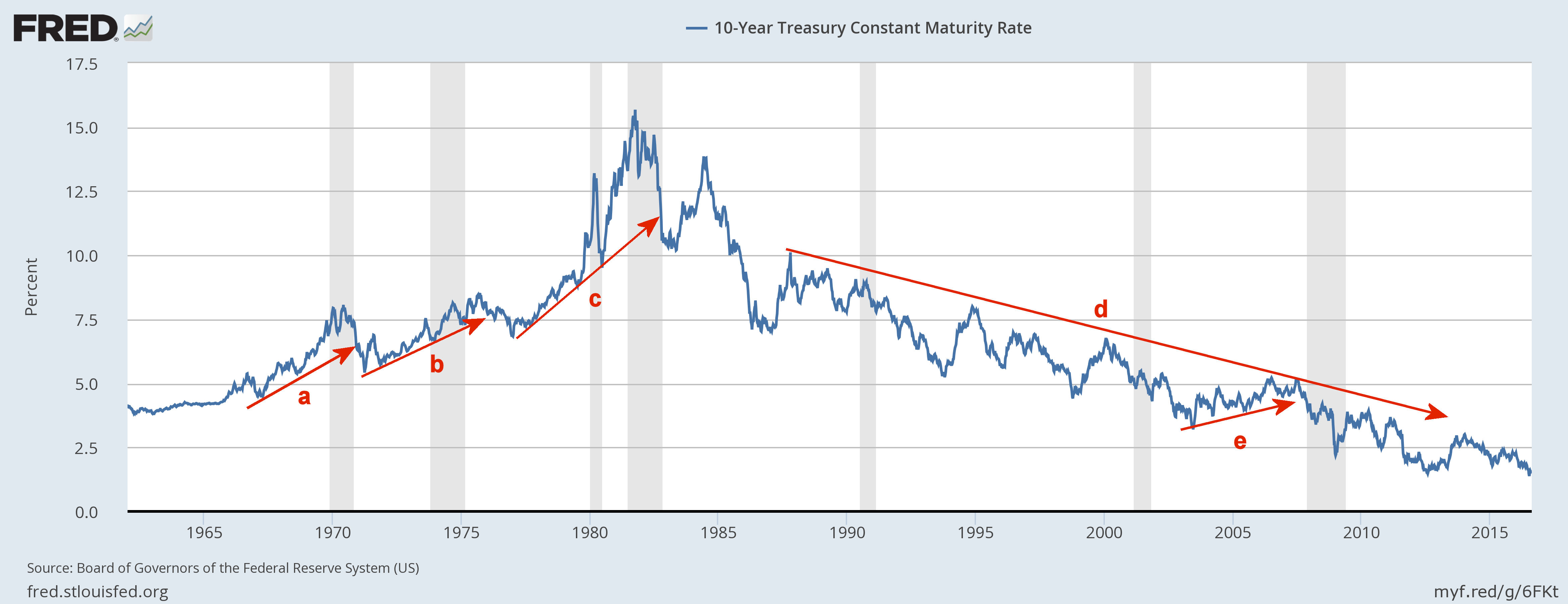

The long-term chart of 10 Year Constant Maturity yields has the recessionary periods shaded in grey. Prior to the recession in 1970 rates had been rising for a number of years, line a. This was also the case during the recession in 1973-1975, line b, as rates continued to rise after the recession was over.

The major rise in rates occurred in the late 1970's as the Fed was trying to fight inflation. The yields finally peaked above 15% as the economy was entering a new recessionary phase. The chart shows that since 1990 yields have been in a well-defined downtrend, line d.

Even during the recessions in 1990 and 2000 rates were still in near term downtrends and yields moved even lower after the recessions were over. The last real tightening period that started in 2004 is just a shallow uptrend, line e, on the long-term chart. This uptrend was broken at the start of the last recession in early 2008.

For a few years I have expressed my concerns that many bond fund and ETF investors are not fully aware of the capital risk in their bond holdings. However I do not think we will see a fast and furious reversal of the major downtrend. I am confident that the technical studies will warn investors in advance of a trend change. In early 2015, the MACD broke its downtrend, line a, which was confirmed by a MACD-His buy signal and signaled higher yields.

From the low at 1.65% yields eventually rose to 2.400% before topping out in July of 2015. By early in 2016 (point 1) it was clear that the downtrend in yields had resumed. In early July the yield closed above the quarterly pivot at 1.474% which was a sign that the rates were stabilizing. The MACD has now crossed above the signal line (point 2) and the MACD-His is weakly positive. The downtrend and 20 week EMA are now in the 1.644% area but as yet there is no strong evidence of a bottom.

The weekly OBV on high yield funds like the SPDR Barclays High Yield (JNK) are still clearly positive and show no signs yet of tipping out. In the past the high-yield ETFS have done a good job of signaling changes in the trend of interest rates. In summary, the bond market is massive and a change in its trend will take time. A weekly close above 2.00% in the 10 year T-Note yield would be the first strong sign of a change in trend.

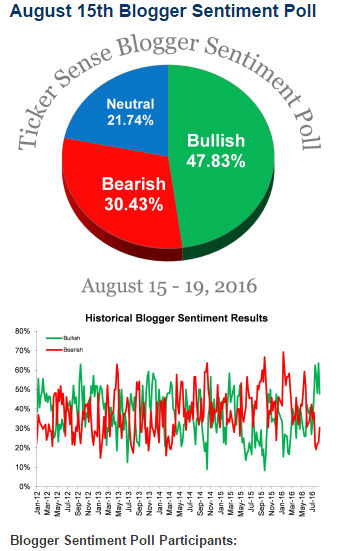

The individual investor was a bit more positive on stocks last week as the bullish% rose 4.3% to 35.6% with the bearish% pretty much unchanged. The TickerSense blogger poll suggests a decreasing amount of bullishness at 47.83% with 30.43% bearish. This is down from its peak of 62.5% from the middle of July.

On June 27th things were much different as only 26.9% were bullish which was not that much different from the 17.4% reading near the February lows. As I always mention the sentiment data must be in agreement with the technical indicators before you take action.

The widely watched but often misunderstood CNN Fear & Greed Index is unchanged from last week at 76 which is extreme greed but it was 90 a month ago. As I have previously pointed out several of the components when they are high and rising indicate strength. It is not until they top out that it turns negative.

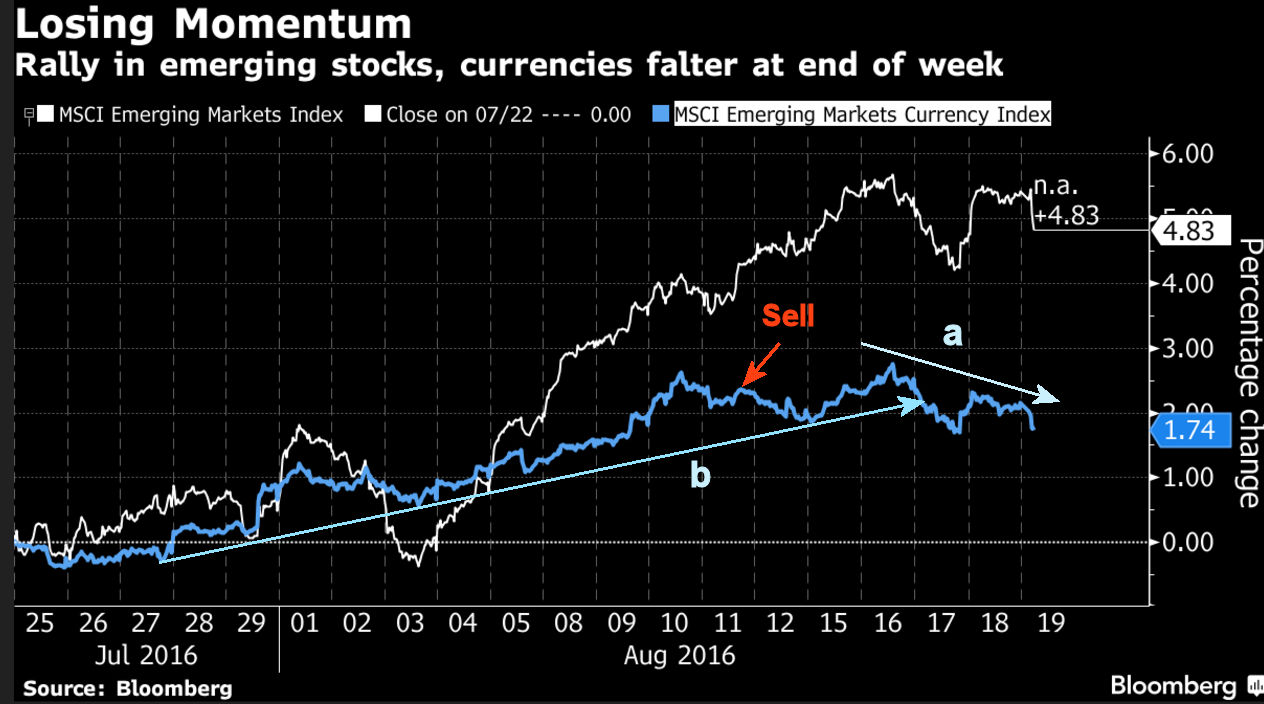

The emerging markets seem to have been added to every buy list over the past week or two but this week's action suggests their timing may be a bit off. This Bloomberg chart shows the MSCI Emerging Markets Index (EEM) and the MSCI Currency Index.

In late July and early August the currency index was in a solid uptrend, line b, while the emerging stock market index had a sharp drop on August 3rd.The uptrend in the Currency Index was broken last Wednesday and as it has started to diverge from stocks, line a.

Any further pullback will be in the context of what does look like a very bullish market. The weekly chart shows that the close on July 15th completed a reverse head and shoulders bottom formation as VWO moved above the neckline at line b. Since VWO broke out there has been little in the way of a pullback. There are projected targets and chart resistance in the $42-$43 area.

The breakout was confirmed by the uptrend in the relative performance and the move above key resistance. The weekly OBV is above its WMA but lagging prices. Viper ETF Traders sold longs in VWO from early July on August 11th for a 10% profit. The daily starc+ bands had been reached as well as one of my upside targets. A more meaningful correction is likely in my view and should provide an opportunity for both investors and traders to buy.

The Economy

It was another week of mixed economic data as Monday's Empire State Manufacturing Survey saw a 4.2% drop while the Housing Market Index at 60 reflects a healthy optimism from builders. On Tuesday, Housing Starts were strong up 2.1% while new permits were flat. There was good news from Industrial Production which jumped 0.7% for the second monthly gain in a row.

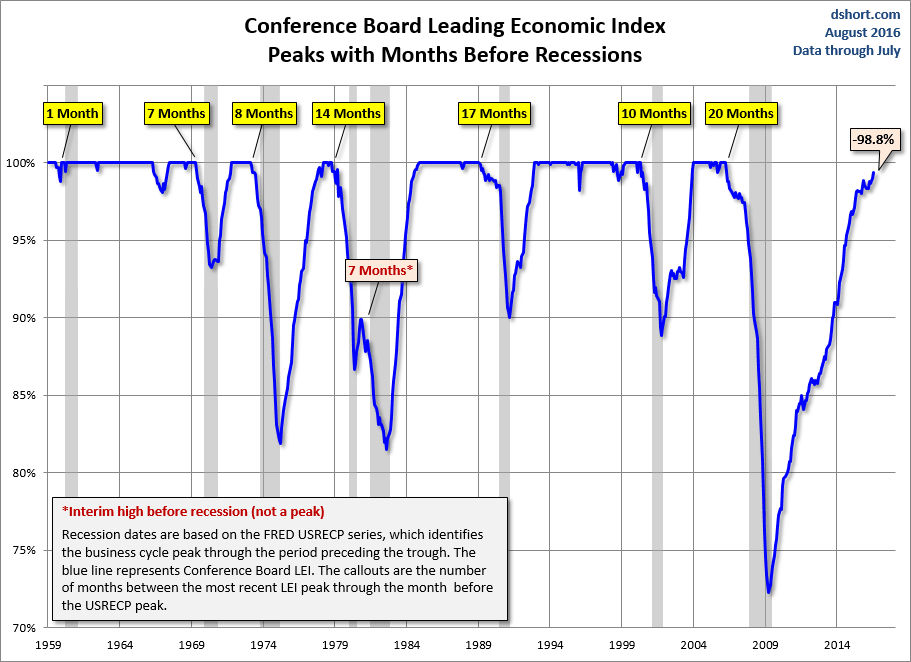

The all-important Leading Economic Index (LEI) rose a healthy 0.4 that was well above estimates. As this frequently featured chart from Doug Short reveals the LEI has a good record of topping out well before the start of a recession. It is unlikely to top out this year as there is a healthy time lag and this supports my positive outlook for stocks. The Philadelphia Fed Survey came in as expected.

On Monday we get the Chicago Fed National Activity Index followed on Tuesday by New Home Sales as well as the Richmond Fed Manufacturing Index. They are followed Wednesday by the flash reading on the PMI Manufacturing Index and Existing Home Sales.

Durable Goods are out on Thursday followed by the preliminary 2nd quarter GDP along and Consumer Sentiment on Friday when Janet Yellen also speaks at 11:00 AM ET.

Interest Rates & Commodities

The sharp drop in the dollar last week is guiding the commodity markets and helps to explain the sharp rise in crude oil just as the majority of analysts were turning bearish and looking for a drop below $35.

In The February 6th column "Is This The Stock Market's Secret Weapon?" I discussed the evidence that the Dollar Index had topped out and what the implications were for commodity prices, emerging markets and earnings.

The recent rally in the dollar has failed below the $98 level and Fibonacci resistance. The close Friday was right on the weekly support at line a. A decline below the $93 level will confirm a resumption of the downtrend with support at $92 and then $90. The weekly Herrick Payoff Index (HPI) dropped below the zero line on Friday indicating the money flow is now negative. The HPI has important support now at line b.

The HPI on the October Crude Oil contract crossed above its WMA on August 4th which was one day after the low in the $40 area. It has now rallied to the $49 level and did form a doji on Friday. There is next resistance in the $50-$51 area with the weekly starc+ band at $52.07.

The daily studies are positive but are getting overextended on a short-term basis which increases the odds of a pullback. This should also be a good opportunity to get back on the long side of the energy ETFs as they have been leading the market higher for the past few weeks.

Gold and gold miners are still in a corrective mode but the weaker dollar should be a positive for both. They could see one more drop if stocks are able to surge to the upside.

Market Wrap

The NYSE A/D line ratios were just slightly positive last week with 1666 stocks up and 1447 down. The Dow Industrials and S&P 500 were fractionally lower but the Dow Transports managed a 1.58% gain. The small and mid-cap stocks did better than the S&P 500.

One again the oil & gas stocks led the market higher gaining 2.1% followed by a 1.7% gain in the basic material stocks. The industrial, financial and technology sectors managed just slight gains while the telecommunications stocks dropped 3.7%.

There are no signs yet of a correction but the narrowing of ranges and the flattening action of the A/D lines suggested to me that the risk on the long side was increasing. Therefore I recommended in the Viper ETF Report last Wednesday that traders should take nice profits on long positions in the SPY, IWM and DIA.

The first sign of a correction would be a 1% or more decline in the S&P 500 that was accompanied by 3 to 1 negative breadth. Until this occurs another push to the upside cannot be ruled out but the potential reward on new longs in the market tracking ETFs does not seem to be worth the risk.

The NYSE Composite dropped to its rising 20-day EMA last week but on both days rebounded to close higher. A new high at 10,876 was made on Monday with quarterly pivot resistance and the daily starc+ band in the 11,000 area. The rising 20 day EMA is at 10,778 with a band of further support in the 10,600-650 area, line a.

The range in the NYSE A/D line has narrowed but is still holding above its slightly rising WMA. A drop below the early August low would be the first sign of weakness. There is more important support at the uptrend, line b, and then at the June highs. The McClellan oscillator failed to overcome the zero level last week and shows a six-week pattern of lower highs, line c.

On a short-term basis the Spyder Trust (SPY) made new highs Monday but closed near the lows. With the selling Tuesday the S&P 500 A/D line dropped slightly below its WMA. It recovered to close the week back above its flat WMA. A decline below the A/D support at line c, would confirm that a correction was underway.

There is resistance for the SPY at $219.50-$220 and a strong close above this level is needed to signal a rally to the $222-$223 area. There is minor support at $217 which if broken should trigger a decline to the $214 area, line a. A close below this level would set the stage for a decline to the $211 area, line b.

The iShares Russell 2000 and the Powershares QQQ Trust (QQQ) are still looking positive technically but the SPDR Dow Industrials (DIA) does show a bit more weakness. Even though the averages did not have impressive gains many stocks did have impressive gains.

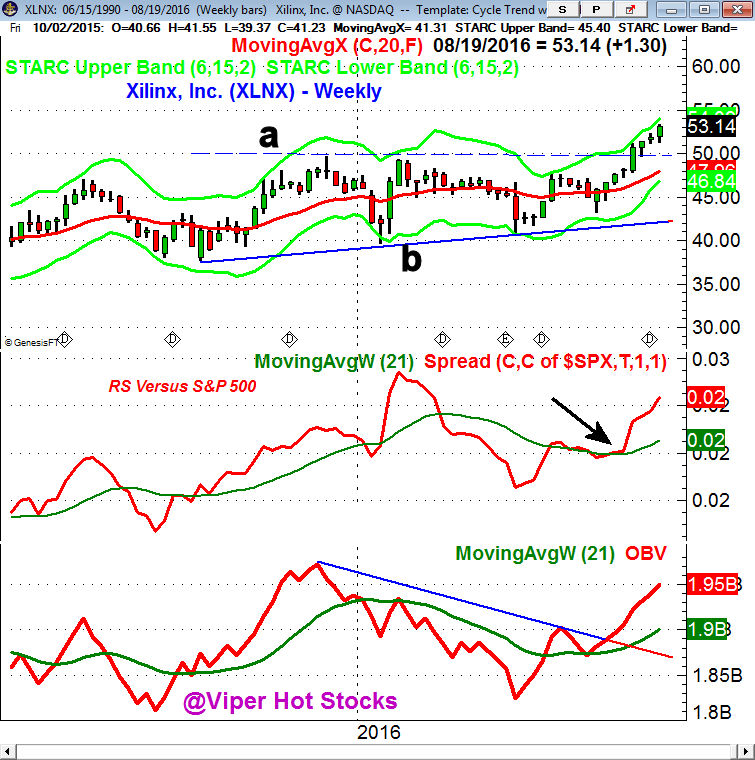

In last week's scan of Nasdaq 100 and IBD Top 50 stocks there were an equal number of new buy and sell signals. Viper Hot Stock traders currently are holding more long than short stock positions. One of our stellar performers was Xilinx , Inc. (XLNX) as it was up 5.5% last week. It had broken out of a major trading range (lines a and b) four weeks ago with next upside targets in the $60 area.

The relative performance and OBV both turned positive before prices broke out to the upside. There are a number of stocks that have either completed major base formations or have broken out of long-term trading ranges like XLNX . These are stocks I will be looking to buy on a correction.

What to do? The failure of the market last week to rally more sharply did turn me a bit more cautious over the short term. A stronger rally is possible this week but in order for me to want again to trade the long side the A/D lines will have to start rallying more strongly.

There has been some increase in bullish sentiment but it seems now that the underinvested professionals are helping to support the market. They are more likely to get caught up in the Fed rate speculation until the FOMC meets in September.

For the past few weeks I have been strongly recommending that investors not be complacent and take the time to weed out any weak holdings from your portfolio. Once the market does start to correct, which seems likely in the next month, those weak holdings are like to decline more than the market. For investors I think there will be a better investing opportunity by October.

In reviewing a number of client portfolios there have been a number of stocks that I felt clients should sell while others I thought had good long-term charts. If you would like our help in reviewing your portfolio please email me at wentworthresearch@gamil.com.

{kind=link}