Those that were frustrated by the stock market's narrow ranges during the summer got more than the bargained for in the past six trading days as the Spyder Trust (SPY) has traded in a wide range. The declines and the rallies have been brief as there have been two days of extreme A/D ratios. It does look as though most of the panic selling occurred on Friday September 9th.

As I expected two weeks ago the Fed chatter has reached a fevered pitch as most analysts seem to be fixated on dissecting every Fed comment. The good news of course is that we will know their decision on Wednesday afternoon which is likely to shift the focus to the next earnings season.

In a September 9th report Factset reported they are looking for a 2.0% decline in 3rd quarter earnings which is lower than their June 30th estimate of 0.4%. Since May I have been expecting that earnings would be better than estimated and that has been the case.

Factset commented that for "Q2 2016, 70% of the companies in the S&P 500 reported earnings above the mean estimate and 53% of the companies in the S&P 500 reported sales above the mean estimate."

I think that earnings are likely to again be stronger in the 3rd quarter which is based on my reading of the sentiment. This would break the negative trend of the past five quarters. Factset is looking for earnings growth of 5.8% in the 4th quarter of 2016 and they expect revenues to increase by 5.3%. Clearly a strong earnings season could be a powerful catalyst to push stocks higher in the 4th quarter.

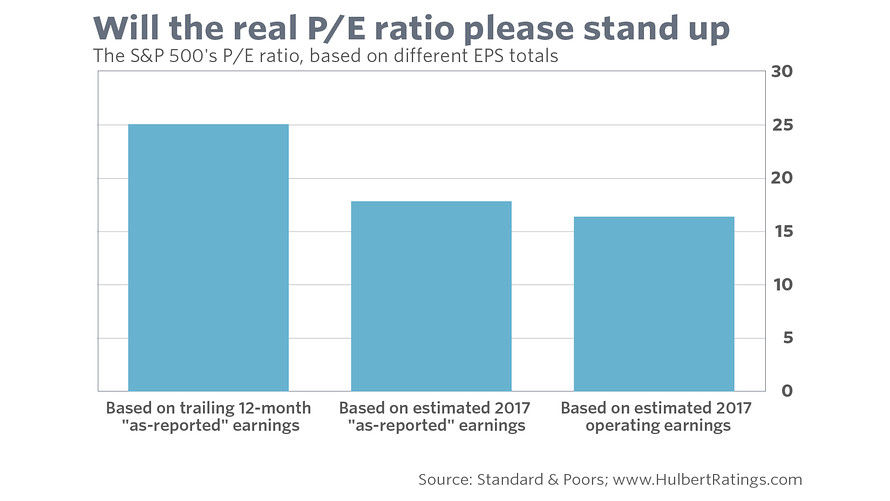

The P/E ratio is a favorite of the fundamental analyst but what earnings value one uses is the source of much debate. It a recent MarketWatch article " Here’s the No. 1 lie the bulls tell about the U.S. market" it is argued that the market bulls who use estimated rather than "as-reported" earnings are masking the market's real overvalued status.

The difference is significant as they point out "Based on trailing 12-month as-reported earnings, for example, the S&P 500’s SPX, -0.44% P/E ratio currently stands at 25.1. In contrast, the P/E is just 16.4 if you focus on S&P’s estimate of 2017 operating earnings."

If you look back to the bearish market articles from 2013 or 2014 very high P/E ratios have often been used by some as a reason why the bull market was ending. With the market's recent sharp drop it is again being used to warn or frighten investors about the stock market. Though there still may be a deeper market correction over the next few weeks there are no technical signs that the bull market is in danger.

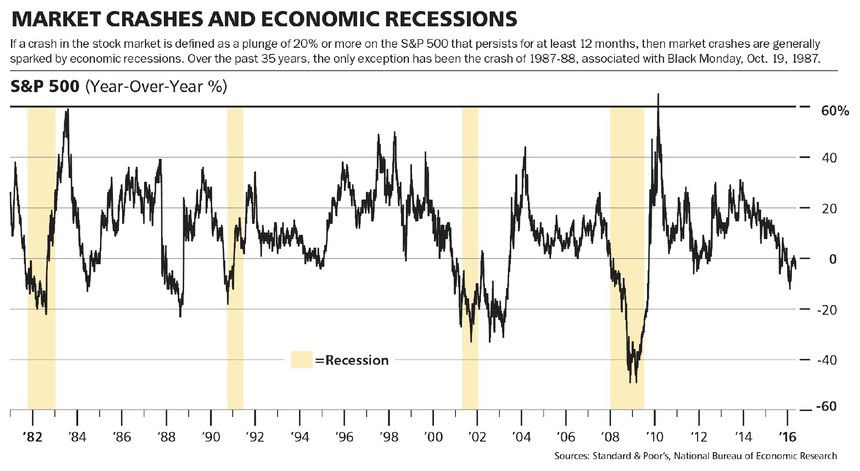

This chart from a May Barron's article shows that market crashes, defined as a decline of 20% or more in the S&P 500, generally coincide with economic recessions. This chart goes back to 1982 and reveals that the economy was already in trouble before most of these crashes.

The exception was the 1987 crash. As I have pointed out before the NYSE A/D line in 1987 formed a significant bearish divergence that warned of the crash well in advance. The market plunge in 2008 occurred after similar negative A/D line divergences and other compelling evidence that the economy was in a recession.

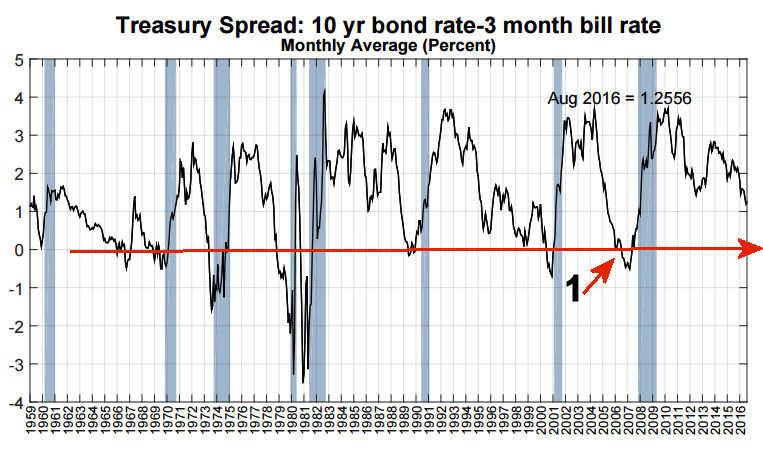

Others are worried that short term rates are rising more sharply than longer-term rates. This long-term chart goes back to the 1950 and notes those times when the 3-month T-BIll rate rose above the yield on the 10 Year T-Note.

This chart plots the spread between the 10 Year T-Note and 3-month T-Bill yields. The declines below the zero line (in red) indentify when the shorter rates exceeded the longer term rates. It has done a good job of warning in advance of past recessions.

In late 2006, point 1, the spread did turn negative which was well below the start of the bear market and the recession. The yield on the 10 Year T-Note closed at 1.701% compared to the 3-month T-Bill yield of 0.289% so the spread is a long ways from turning negative.

Should you care if the P/E ratio is too high or that the market bulls are misleading you?

As someone who has studied and analyzed the stock market for many years I do not have much faith in reported earnings and even less in estimated earnings. I see them as a lagging not a leading indicator.

Technical analysis depends on how the market has priced a stock or ETF in the past and how it is pricing it now. Therefore I would not pay much attention to the P/E ratios or how they are calculated as the A/D line analysis has a much better record of identifying bull market tops than any fundamental measure.

Last week we had a good example of the difference between fundamental and technical analysis. Starting last week the reviews on the new iPhone and the outlook for sales were not that optimistic. Several media traders were also negative on the stock but it is apparent that they do not really look at the charts. Long gone are the days when CNBC had a great technical analysts like John Murphy on their staff.

As I commented in the September 6th Viper Hot Stocks report "In early August I noted the improvement in the monthly and weekly studies for Apple, Inc. (AAPL). This was a sign for me that I would be looking for a correction to buy. The official launch of their new phone is Wednesday night but even if it is not well received the long side is still favored as the technicals do favor buying."

At the time the weekly chart revealed that there was major converging support in the $102.40 area and the rising 20 week EMA. I was not sure that we would get that deep a correction as AAPL had just traded over $110 and therefore I was looking to buy at $107.14/$105.86.

Both levels were hit on September 8th and on last Monday the stock plunged to a low of $102.53 which was just below the 38.2% Fibonacci retracement support at $102.83. AAPL dropped well below the starc- bands, point 1. This was a sign it was in a low risk buy zone. It has been quite a week for AAPL as it had a high of $116.13 before retreating slightly on Friday. Traders took a 50% profit at $115.66 but the next upside target is at $120.

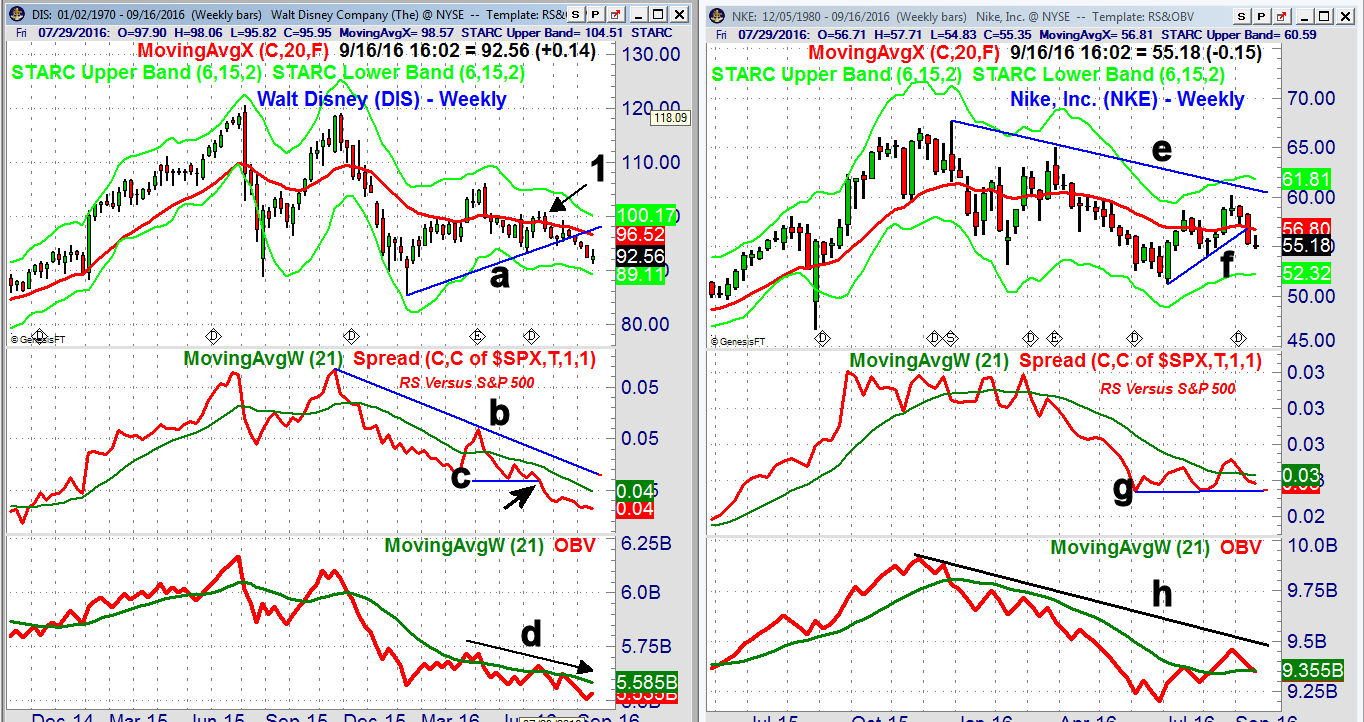

Instead of analyzing why they had not bought AAPL the traders started a long disucssion on whether Disney (DIS) down 11.2% YTD, or Nike (NKE) down 10.5% YTD, looked better. DIS generated a weekly doji sell signal in July (point 1) and was recommended on the short side. Four weeks later the support at line a, was broken as the RS line had already violated its support (line c). The OBV shows a pattern of lower highs indicating that the decline is not over yet.

Nike (NKE) has been acting a bit better recently as it has rallied from the July low at $51.33. The ABC rally from the lows looks more like a rebound in the downtrend as it failed at the 50% retracement resistance of the decline from the December 2015 high. The uptrend line f, was broken a week ago and NKE is still in a long term downtrend (line e).

The weekly RS is back below its WMA but the RS is still above the support at line g, so it could be completing a bottom. The OBV closed the week just below its WMA but is still trading well above the recent lows. From a technical perspective I see no compelling reason to buy either stock.

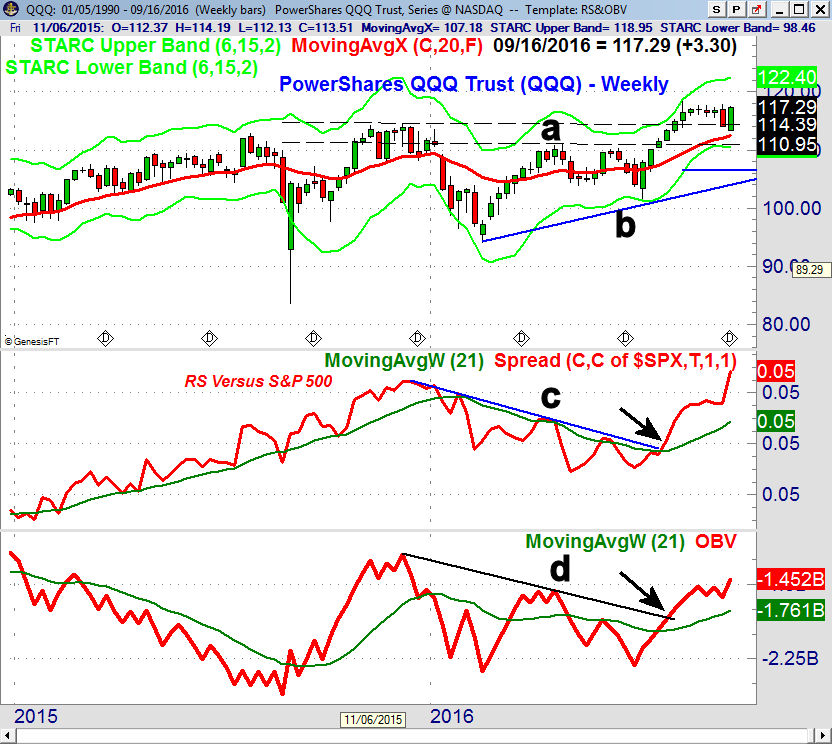

So once the FOMC fog clears this week the market may resume its push to the upside. On the next rally what sectors look the best from a technical perspective? The PowerShares QQQ Trust (QQQ) seems like an obvious choice as it has a 10.5% holding in AAPL but I do not think that is the whole story.

The QQQ was up 2.8% last week versus a 0.53% gain in the S&P 500. The weekly chart shows that the low this week at $113.35 was right in the middle of its support zone, line a. The relative performance broke its downtrend, line c, in late July and soon confirmed that QQQ was a market leader. It has accelerated to the upside over the past two weeks. The weekly OBV also looks strong as it made a new high for the year last week.

In addition to the tech sector the Nasdaq 100 also has a high concentration of biotech stocks. The SPDR S&P Biotech (XBI), like the QQQ, was also recommended to Viper ETF clients, and it was up 5.7% last week. It closed the week at $64.71 and the next major targets are in the $69-$70 area. There are other sectors like the transports and retail stocks that need a sharp rally to complete their corrections.

The Economy

The data last week did not help clarify the economic outlook as there were more signs of weakness that will make it less likey the FOMC will raise rates. The market is also nervous about Wednesday's Bank of Japan meeting and it does seem likely they will take some action.

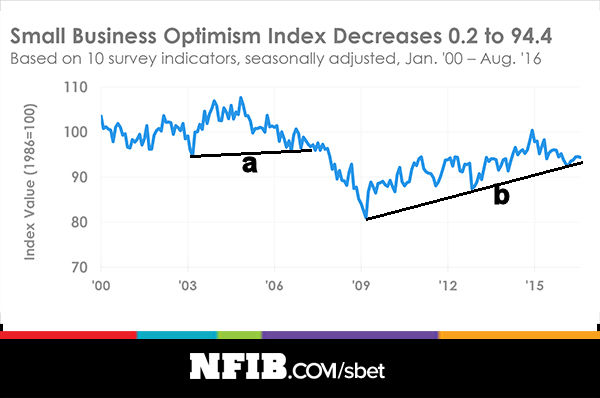

The NFIB Small Business Optimism Index came in as expected but is now testing support at line b. The survey indicated that "Small business owners are reluctant to expand, expect worse business conditions and are unable to fill open positions." The chart shows that a break of multi-year support, line a, in 2007 warned of the coming recession.

In contrast Thursday's Philadelphia Fed Business Outlook Survey came in much stronger than expected at 12.8 as the market expected 2.0. Another higher reading next month should confirm a new uptrend. The Empire State Manufacturing Survey is still negative but did improve from the previous month. Industrial Production was negative as it reversed July's gains. Retail Sales were also weaker than expected on Thursday and inventories were unchanged.

The 0.2% gain in the Consumer Price Index was a surprise but was not likely strong enough to change the Fed's view of the economy. Clearly higher inflation would be a positive for the economy and the stock market. The Consumer Sentiment came in at 89.8 and was unchanged from July's final reading.

This week we have the Housing Market Index on Monday followed on Tuesday by Housing Starts. The Wednesday afternoon FOMC announcement will clearly get the most attention and it is likely to cause another spike in volatility.

The data continues on Thursday with the Chicago Fed National Activity Index, Existing Home Sales and also the important Leading Indicators. Friday's flash reading on the PMI Manufacturing Index may shed more light on the health of the manufacturing sector.

Interest Rates & Commodities

The yield on the 10 Year T-Note rose again last week to 1.701% and is now close to the resistance from early in the year at 1.750%. Volume in some of the high yield ETFS, like the SPDR Barclays Capital High Yield (JNK) was heavy last week but JNK was flat for the week. The weekly OBV on JNK is still positive.

The November Crude Oil Contract lost almost $3 per barrel last week and there is next important support in the $51.50-$42 area. Gold was also hurt by the stronger dollar as it dropped $24 and is now close to the more important support in the $1300 area.

Market Wrap

For a wild week the S&P 500 managed a 0.53% gain which was slightly better than the 0.46% rise in the small cap Russell 2000. The Dow Utilities led the major averages up 2.38% while the Dow Industrials were up only 0.21%. The NYSE Composite and Dow Transports were lower, losing 0.77% and 0.67% respectively.

For the second week in a row the declining stocks led the advancing stocks with 2048 down and 1062 up. Therefore it is a good time to look at the A/D lines across all time frames. The monthly NYSE A/D line is still well above its rising WMA after it signaled the upside breakout in May.

The monthly A/D line dropped below its WMA in December 2007 just after the market's high and was negative by early 2008. The weekly NYSE A/D line (not shown) has been declining for the past two weeks but is still well above its rising WMA.

The Spyder Trust (SPY) had a low last week of $211.34 which is still above the starc- band at $209.77 with more important weekly support at $207.60, line a. The quarterly pivot is at $206.88. The S&P 500 A/D line was flat last week but is above its rising WMA. There is more important A/D line support at line b. The OBV made a new high last week as it broke out to the upside (line c) in July.

The NYSE Composite is acting weaker as it is testing the support, line b, that goes back to early in the year. The daily starc- band was tested early in the week with initial resistance at 10,710 and the declining 20-day EMA. The quarterly pivot stands at 10,352.

The daily NYSE A/D line rebounded back to its WMA last week after dropping below short-term support, line c, early in the week as it now looks corrective. There is more important support at line d, and the August low. The McClellan Oscillator closed at -126 and has key resistance (line e) at the zero line.

The daily Dow Industrial A/D line also looks corrective but the weekly A/D line is above its WMA. The daily Russell A/D is barely above its WMA but the weekly A/D line did turn up last week. The weekly Nasdaq 100 A/D line also rose last week and is still well above its strongly rising WMA. The daily Nasdaq 100 A/D line is now in a range and could break either way.

What to do? The stock market could break either higher or lower in the next week. Most are expecting stocks to rally if the FOMC does not raise rates. Since this is the prevailing opinion it may not happen. If we do see a break of the recent lows, then the S&P 500 could easily decline to the 2080-2100 area where I expect there to be good buying.

Even though the economy still shows some signs of weakness there are no signs yet of a recession. Therefore I am still looking for a strong market as we head into the end of the year but I cannot rule out some further choppy action over the next few weeks.

Before we see a major decline of over 10% or a bear market I would expect to see some clear warnings from the A/D lines. Therefore I think stocks are the best place to be in the fourth quarter.