The widely anticipated monthly jobs report on Friday shocked forecasters as for the second month in a row they were way off the mark. In the June report May's numbers were revised even lower to just 11,000 new jobs.

The 285,000 reading for Non-Farm Payrolls was above even the most optimistic CNBC forecast and the increase of 38,000 jobs in professional and business services was especially encouraging. Even manufacturing had a gain of 14,000. Still it is not surprising that some who have been warning about the deterioration in the economy were still not impressed.

The Non-Farm Payrolls chart suggests the trend may have changed with the June report but one should remember that this data series, like many of the economic reports, is subject to wide swings on a month-to-month basis. Many economists are more concerned by the fact that S&P 500 came within a fraction of the all time high and yields on the 10 Year T-Note dropped to new all time lows.

Technical indicators like volume, price as well as the number of stocks advancing or declining are rarely revised and this is one of the many reasons I favor technical over fundamental analysis. As I pointed out last week the fact that the A/D lines on the major averages did not make new lows during the post Brexit market decline was a sign of strength.

Friday's gains were impressive as the major averages were up 1.5% or more and even more important there were 2711 stocks advancing and just 370 declining. The strength of rally was likely fueled in part by short covering as even after the close one long time market bear called the market's reaction "comical".

The continued disbelief in the market rally is a bullish sign. The weekly chart of the Spyder Trust (SPY) shows that the S&P 500 Advance/Decline line moved back above its WMA on February 26th and the SPY has gained 10% since the A/D analysis again turned positive. It made another strong new high this week as it continues to lead prices higher. Those who have been following my analysis throughout the bull market know that this analysis is what I use to determine whether I am buying or selling stocks and ETFs.

Even though many of the major averages have just made it back to their pre-vote levels many stocks have done much better. Two of the recent Viper Hot Stocks picks, CBOE Holdings (CBOE) and Paychex (PAYX) were identified as market leaders before the vote and are now 4.8% and 8.3% above their pre-vote levels.

Since the Brexit vote my inbox has been deluged daily by 6 or 7 times the average number of financial articles and for a while I thought my spam filter had been turned off. A very high percentage of the articles expressed a pessimistic view on the stock market and/or the economy.

Many focused on the dire consequences of the recent vote and how it must doom the Euro zone economies and lead to a global bear market. They may be right eventually but since the vote it has become clear that no one really knows how the UK exit from the European Union will pan out. There will probably not be clarity on this issue until next year and there is the potential for things to change significantly before the split is final.

Others are taking the view that the very low rates in the US and negative rates in other parts of the world are warning of an economic slowdown and an eventual collapse of equity prices. Those who are worried about the deflationary implications of low rates also believe it has to be negative for stock prices.

When I see one of these articles I will often take the time to read them and assess their argument. I also take the next step as I suggested in a column several weeks a ago " Look Before You Leap" to look back at past comments from the author. I tend to pay more attention to an analyst's warning if they had been positive on stocks for most of the bull market. On the other hand those who have been making the same arguments for 2-3 years are treated with more skepticism.

I have been analyzing the stock market since the early 1980's and think I have gained insight from each bear market. I have also extensively studied past bear markets and my research has shown that over time there have been very few analysts or traders that have recognized the start of past bear markets. The current flood of articles seems to be driven by a race for the bragging rights once the bull market tops out..

If you study the market's history you will find a number of comments near bull markets highs that are extremely similar. The 1973-1974 bear market was the most devastating since the depression as some widely held mutual funds dropped over 70% (See Kiplinger article) Very close to the early 1973 highs Barron's ran an article titled, "Not a Bear Among Them" to describe the bullish consensus of institutional investors.

After the market had dropped 15% in 1973 Treasury Secretary George Schultz commented that there were "bargains galore" that he was not able to buy because of his position. Then in August 2007 which was just two months before the market topped out " Treasury Secretary Henry Paulson explained that U.S. subprime mortgage fallout remained largely contained due to the strongest global economy in decades". Don't expect many to correctly identify the next bull market top.

As is evident on the charts the subsequent declines were quite devastating if you were on the wrong side of the market. In both cases the market internals warned of a top in advance and as I noted in early June the new high in the monthly A/D line sent a very bullish message about our current market.

Most of the bear market forecasters base their analysis on fundamental data such as price to sales , P/E ratios, high margin debt, etc. Those that use technical analysis try point out divergences between the US market and Chinese stocks or some other market that they feel is more important than the US stock market. The dismal performance of the hedge funds over the past few years has shown that most of these macro strategies do not yield profits

The strongest argument in favor of technical analysis is that if applied objectively it can tell you objectively when you are wrong. This is what is missing from most of the bear market forecasts is that they do not have an exit strategy. These authors rarely provide an objective way to determine that their analysis was wrong. They are therefore stuck with their market forecasts no matter how high a market goes.

This chart from last September was designed to illustrate how the level of bearish market commentary often peaks near a market 's correction low. In May 2010 an Economist article highlighted some of the market's concerns as they said " Fears are growing that the global recovery will falter as Europe's debt crisis spreads, China's property bubble bursts and America's stimulus-fuelled rebound peters out. " Does this sound familiar six years later?

Even in 2010 investors were cautioned about stocks because of a fear over deflation but just a few months later (red arrow) the S&P 500 had surpassed the 2010 high. This was an objective way to get back in the market's rising trend.

Once again in the summer of 2011, US debt was downgraded and many thought we were starting a new recession. By October 13th "Be Bold, Be Fearless...Buy the Dip" there were clear signs that the market had bottomed based on the A/D line analysis but the S&P 500 did not make new highs until early 2012.

Those who were bearish in 2011 had an opportunity to switch back to the long side had they used a stop. I have noted additional points on the chart where using a stop above the previous high would have again confirmed the major trend.

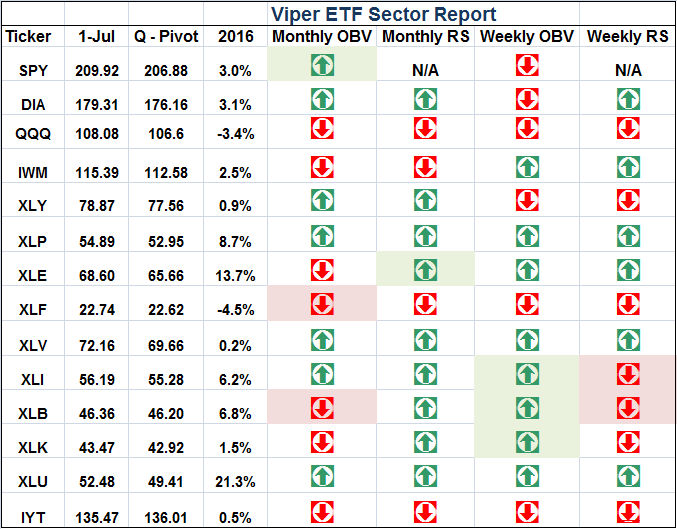

As I discussed last week "The Investors Best Crisis Strategy" comparing weekly closing prices to the quarterly pivots can often be helpful in allowing one to stay in a major trend. The table from last week's Viper ETF Report has the new quarterly pivots for some of the major ETFs.

The Economy

Though many are talking about an imminent recession the economic indicators that I watch are not sending any warning signals at this time. One of my favorites, the Leading Economic Index, shows no signs of a top and it will next be reported on July 21st.

The short holiday week most of the data, like the monthly jobs report, was better than expected. The PMI Services Index was about as expected the ISM Non-Manufacturing Index at 56.5 was much stronger than 53.3 which was the consensus estimate. Factory Orders declined but met consensus estimates.

The calendar is light this week with the Producer Price Index on Thursday along with jobless claims. It is followed on Friday by the Consumer Price Index, Retail Sales, Empire State Manufacturing Index, Industrial Production, Business Inventories and Consumer Sentiment.

Interest Rates & Commodities

As the yield on the 10 Year T-Note has dropped to a new all time low the most prominent bond fund managers, including Bill Gross and Jeffrey Gundlach, do not expect rates to drop much lower. Gross is shorting high yield bonds and does not think the jobs report will spur the Fed to raise rates. Both are also quite negative on the stock market. The fact that yields have reached the daily and weekly starc- bands in my opinion does favor at least a short-term reversal in yields.

The acceleration of gold to the upside over the past month has left me on the sidelines but I am still not willing to chase prices as the gold futures approach $1400 and the weekly starc+ band. The weekly studies are positive on gold while the daily indicators do show some divergences.

The latest data from the CFTC shows that the long positions of money managers have made another new high even though margins were recently raised. In my experience this is a dangerous combination and I continue to think the long side is risky now.

Crude oil has dropped down to test the minor 50% support level on Friday as last week's inventory data pushed prices lower. A strong rally early this week is needed to indicate that a short term low is in place. Using the methods discussed in Friday's Viper Trading lesson a rally in crude would have upside targets in the $54 area.

Market Wrap

The major averages were led on the upside by the 1.9% gain in the Nasdag Composite which was followed by the 1.8% rally in the small cap Russell 2000 and the 1.6% gain in the Dow Transportation Average. The S&P 500 was up 1.3% and on the week the advancing stocks led the declining ones by a 2-1 margin.

In the latest AAII survey individual investors were a bit more bullish at 31.1% up 2.1% in the last week. The most significant change was the 6.8% drop in the % of bearish investors. The VIX has dropped back to 13.20 and is very close to the June lows. According to option expert Larry McMillan his analysis of the put/call ratios is bullish.

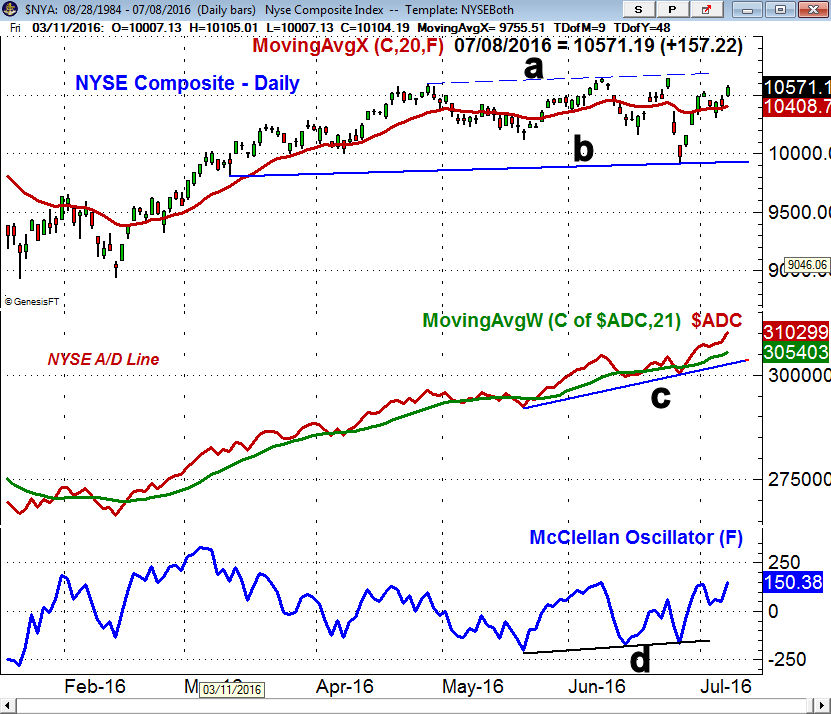

The NYSE Composite gapped higher Friday but is still within its trading range, lines a and b. A completion of this range would have upside targets in the 11,200 area and the May 2015 highs. The NYSE A/D line broke out to the upside over a week ago and closed Friday at another new all time high.

The A/D line has first good support at line c, with more important at the May low. The McClellan oscillator formed a bullish divergence at the post vote lows, line d, and is now in a short-term uptrend. The 20 day EMA is at 10,400 with the quarterly pivot at 10,352.

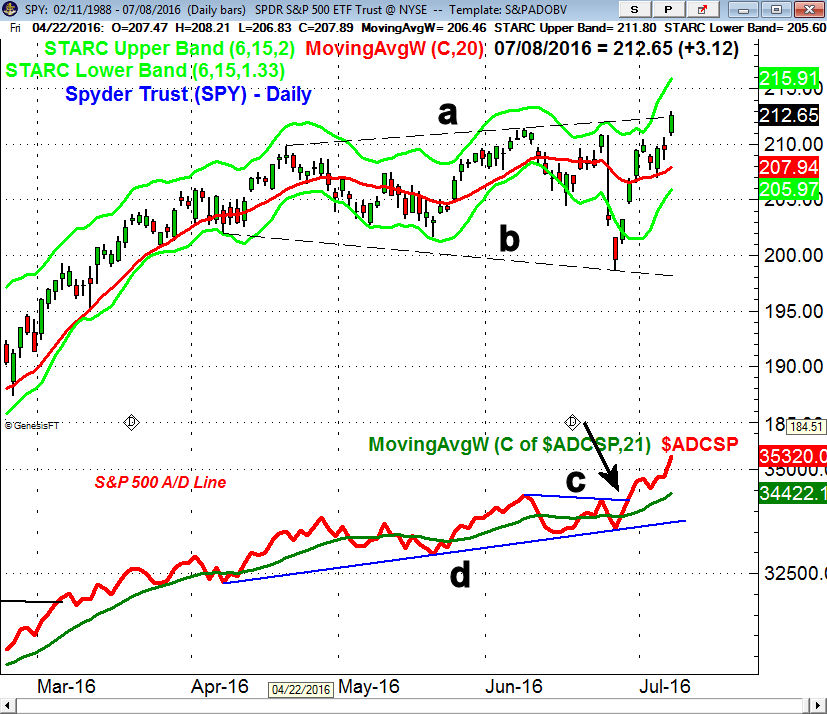

The Spyder Trust (SPY) closed just slightly above the resistance at line a but further gains are needed to confirm the completion of the trading range (lines a and b). The initial quarterly pivot resistance is at $215.11 with the daily starc+ band at $215.91. The trading range has upside targets in the $218-$222 area. There is initial support now in the $210 area with the 20 day EMA at $207.94. The quarterly pivot stands at $206.88.

The S&P 500 A/D line closed the week very strong as it held the support at line d, on the post vote drop. The move through resistance at line c on June 29th forecasted a new high for the SPY. The A/D lines for the IWM, DIA and QQQ have all moved to new highs and confirmed the price action.

What to do? The market correction last week was shallower than I expected and the strong weekly close made it a tough week for the bears. More pain is likely for them this week as a new closing high in the widely watched S&P 500 is expected. Nevertheless we should see a decent pullback in the next week or so that should be another buying opportunity.

The next significant target for the S&P 500 is in the 2180-2200 area and I continue to favor stocks over bonds. Investors should continue to favor positions in low cost, broad based ETFs or mutual funds.

As I mentioned a few weeks ago I think this earnings season may be much better than most expect. If this is the case it could help to bring some of the vast amount of cash on the sidelines back into the stock market. Viper ETF clients established long positions last week in the SPY, IWM, DIA, XOP and VWO.

{kind=link}