The market continued sharply higher to start off the holiday shortened week and for three consecutive days the gains were impressive. This was enough to get the market's and investor's attention. There were signs early Thursday that the rally was stalling which was supported by the weak technical nature of crude oil.

This was a good example of why it is important to look at more than the price action before taking action. April crude oil had rallied over 17% between the prior week's low and Wednesday's close but as I noted in Thursday's Viper ETF Report " the OBV is still weak . Therefore I would not chase the long side at current levels as a pullback is likely going into next week."

The United States Oil Fund (USO) opened 2.8% higher Thursday before reversing to close on the lows. The SPDR Oil & Gas Exploration ETF (XOP) gapped below the previous four days lows on Friday and trapped the late buyers on the long side. Despite the short term weakness there are signs that crude oil and the energy stocks are bottoming.

The stock market rally was what I was looking for in last week's "Is There Blood In The Streets Yet?". The negative sentiment and multiple oversold readings from a number of market measures needed a burst of upside momentum to reverse the market's downtrend. The strong price gains along with strong market internals was enough to do it.

The S&P 500 A/D line overcame the resistance at line c, which confirmed the bullish divergence (line b) that formed at the February 11th lows. This is consistent with a further rally after the market completes its short term period of consolidation. This should take SPY to new highs for the month with next targets in the $196-$198 area. This of course first requires a move in the S&P 500 cash above the widely watched 1950 level.

The S&P 500 A/D line overcame similar resistance last October, line a, on October 7th as the SPY rallied into early November gaining 6%. In October the A/D line continued to rise sharply after overcoming resistance as it started acting stronger than prices.

The market action this week is therefore quite important and the A/D line needs to overcome the resistance at line d, to signal that an intermediate term low is in place. The market does need to move significantly higher to reverse the massively negative bearish sentiment as while many investors have fled the markets many traders are still holding many puts. A high level of negative sentiment is needed to propel the market even higher.

Watching the sentiment as the current rally develops will be important. If the sentiment reverses too quickly then it could send a warning that the market's upside momentum is waning.

In today's article I would like to discuss three sentiment indicators that investors and traders should follow. All are available online but it is important to remember that market sentiment must be combined with technical analysis in order to identify important turning points.

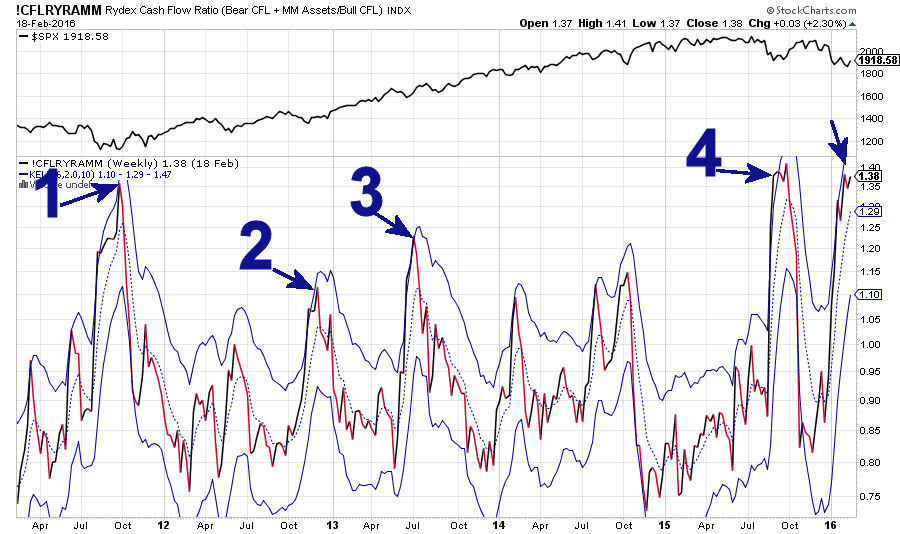

Many of you may be familiar with the Rydex funds as they were one of the first to introduce bear funds. The Rydex Inverse S&P 500 Strategy fund (RYURX) was one of the few alternatives before the introduction of inverse ETFs. One way to use these funds as a sentiment indicator is through fund flows.

Well known technical analysis and founder of Decision point Carl Swenlin introduced this data in 2004 and his company was merged into stockcharts.com in 2014. He has his own unique analysis of this data and more can be found here.

The chart was created using the weekly data on the Rydex Cash Flow Ratio (Bear CFL + MM Assets/Bull CFL) which you can follow on stockcharts. I have overlaid my starc bands analysis on the chart in order to identify extremes. I have highlighted several instances when this ratio has reached or exceeded the starc+ band.

On September 26th 2011, one week before the market bottomed, the ratio closed at its starc+ band (point 1) Three weeks later the ratio dropped below its 6 week SMA as market began to rally more sharply.

The ratio also came close to its starc+ band (point 2) in late November of 2012 as fears over the fiscal cliff and the re-election of President Obama caused a sharp increase in bearish sentiment. In May of 2013 the S&P 500 started a month long correction as the ratio expanded sharply to move above its starc+ band on July 1st, 2013 (point 3). This happened even though the market had already started to rally.

The ratio also reached sharply higher levels on September 8th 2015 as it closed above its starc+ band (point 4). The ratio stayed at high levels until October 12th when as it began to drop sharply. On January 19th the ratio again closed above its starc+ band (see arrow) and it is still trading near its high. A weekly drop below its SMA at 1.29 will be a sign that the fund flow has changed. If the ratio moves then back below 1.00 it will be time to watch the market action more closely.(Here is a link for my chart)

In the latest survey from AAII the bullish% jumped 8.3% to 27.6% after reaching a low the prior week of 19.6%. Just after the January lows I noted in ("Is Bullishness Low Enough Now?" ) that it had dropped to 17.9% which was the lowest reading since 2005. The long term average is 38.6% and once the bullish% moves back above 40% I will be looking for any technical signs the market's rally is stalling.

The Put/Call ratios have been very high for some time as they reflected a high amount of put buying and therefore a high degree of bearish sentiment. The Option Strategist's Larry McMillan, who I have known for 30 years, is one of the top option analysts. In his recent analysis he commented that "Both the equity-only put-call ratios and the Total put-call ratio gave buy signals on Wednesday, February 10th – one day before the lows."

The Put/Call ratio is one of the seven components of CNN's Fear & Greed Index . Just one week ago it was at 21 and a month ago was very low at 9 which was well in fear territory. It is currently neutral at 49 and is likely to move higher over the next several weeks. It would not be surprising for it to get to the 75-80 level as the market moves higher .

By following these three measures of sentiment one should be able to gain some insight on when the market sentiment has changed from being too bearish back to more historically neutral levels. At that point it will be important to closely analyze the market technically to see if it's trend is changing.

The pullback late in the week is likely a buying opportunity and as I discussed last week " Charting Barron's High Yield Industrial Picks" there are several of the big, high yielding industrial stocks that look positive based on the weekly/monthly technical studies.

There are obviously also a number of very oversold stocks which are likely to rebound but do not yet show signs of an important low. Some stocks that had a rough 2015 like Whole Foods Market (WFM) appear to have bottomed. It was down 32.5% in 2015 but it was recommended last week to clients of Viper Hot Stocks.

The chart of WFM shows that it traded in a tight range over the past month and then closed on February 12th above the doji high. Though WFM did drop below the late 2015 lows in the past month the relative performance (line b) and the on-balance-volume (OBV) (line c) both formed bullish divergences as they did not make new lows with prices. They are now above their WMAs and on a move above the resistance at $35 WFM should run to the $40-$42 area.

The Economy

There were a few bright spots last week from the economic data but overall the data on the manufacturing sector is still weak. The Empire State Manufacturing Survey came in at -16.64 much weaker than the -10 consensus estimate. The Philadelphia Fed Business Survey was a bit better than expected but still weak at -2.8.

The Housing Market Index also dropped to 58 which was down from the prior reading of 60 but well above the key level of 50. According to Econoday it is still " signaling that confidence among the nation's home builders is very strong". Housing starts were down a bit in January but still up 6.4% on a year to year basis.

The Industrial Production was surprising strong in January up 0.9% but is still negative on a year to year basis. This was the best monthly reading since 2014 and another positive reading for February would be a good sign.

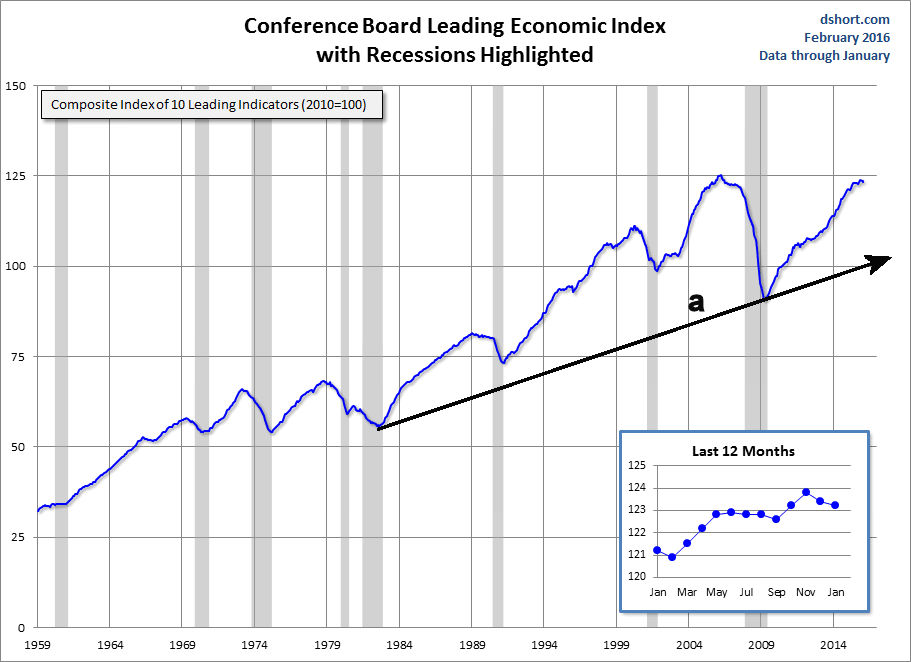

The all important Leading Economic Indicators was down 0.2% in January. According to the Conference Board's Ataman Ozyildirim “The U.S. LEI fell slightly in January, driven primarily by large declines in stock prices and further weakness in initial claims for unemployment insurance".

As I have noted in the past this indicator has an excellent record of topping out before the start of a recession. This chart (courtesy of dshort) shows that the long term uptrend, line a, is still intact. However from the insert one can conclude that a decline below the low from last September would be a reason for concern.

The CPI on Friday reflected a 0.3% jump and the recent evidence of wage inflation is a good sign for the economy. It could give the Fed some room to raise rates later in the year. The minutes from the last FOMC meeting did show increased concern over the strength of the economy.

The economic calendar is full this week with the Chicago Fed National Activity Index Monday along with the Flash PMI Manufacturing Index . Then on Tuesday we have the S&P Case-Shiller HPI, Consumer Confidence, Existing Home Sales and the Richmond Fed Manufacturing Index.

We get a new reading on the services sector Wednesday with the Flash PMI Services Index and also New Home Sales. This is followed on Thursday with the Durable Goods and jobless claims. The week finishes with the latest reading on 4th quarter GDP, Personal Income and Outlays along with Consumer Sentiment.

Market Wrap

The Dow Transports and small cap Russell 2000 led the market higher last week with gains of 3.4% and 3.9% respectively. The S&P 500 and Nasdaq Composite gained 2.8% while the Dow Industrials was up a bit less. Very solid A/D numbers as 2683 stocks advanced while only 516 declined. Only 116 NYSE stocks made new lows last week versus 978 the previous week.

Though the daily outlook on the Spyder Trust (SPY) has clearly improved the more broadly based NYSE Composite is still lagging. On the weekly chart the drop below the weekly starc- band five weeks ago was clearly significant.

The resistance from four weeks ago at 9651 is the key level that needs to be overcome. Once it is the declining 20 week EMA at 9890 is the next key barrier. It corresponds to the lows from late 2015 (dashed line). The weekly starc+ band is is at 10,156.

The weekly A/D line has turned up after breaking support, line d, in January. The A/D line now needs to overcome its WMA and the downtrend, line c, to signal a stronger rally. The weekly OBV has also turned higher but so far the volume on the recent rally has not been impressive. A move in the OBV above the previous peak would be a good sign.

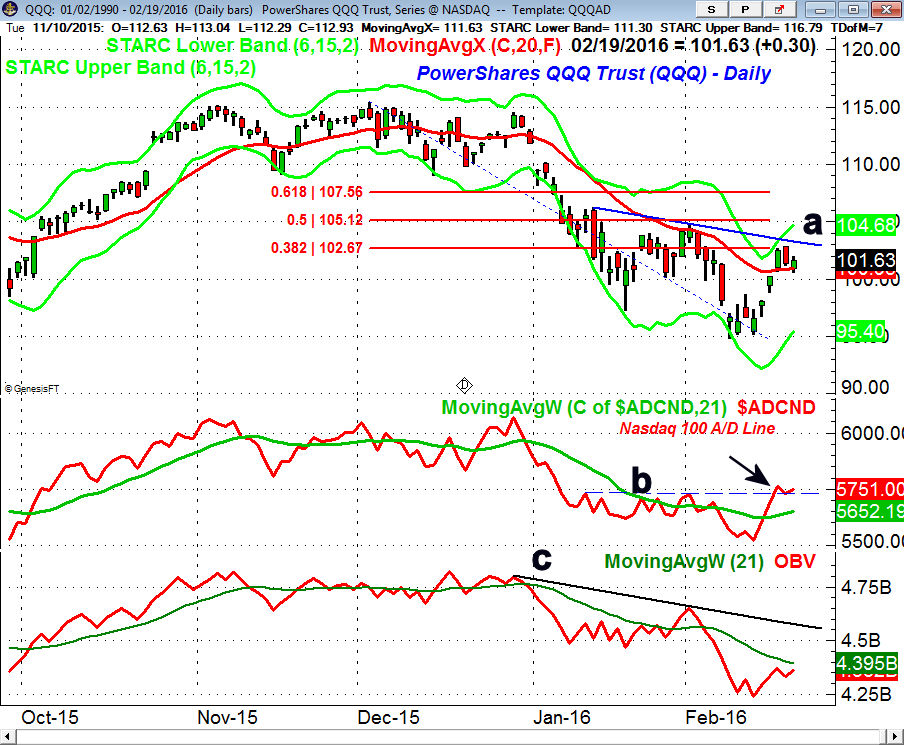

The PowerShares QQQ Trust (QQQ) which tracks the Nasdaq 100 had a good week as it was up 3.7% for the week. The weekly doji formation on the iShares Nasdaq Biotechnology (IBB) I mentioned last week did suggest a bottom might be forming. This week's close above in IBB above the doji high indicates it still can move higher along with the health care sector.

The daily chart shows that the QQQ has just reached the 38.2% Fibonacci retracement resistance and the downtrend, line a. The 50% resistance is at $105.12 with the more important 61.8% level at $107.56. There is still a major band of resistance on the daily chart in the $109-$110 area.

The Nasdaq 100 A/D line did not form any positive divergences at the recent lows but was able to overcome key resistance, line b, last week. This does favor a further rally and the WMA of the A/D line is now rising. The daily OBV is still below its WMA and the resistance at line c.

The SPDR Dow Industrials (DIA) shows the best monthly and weekly relative performance as it is leading the S&P 500 higher. The bullish divergence in the Dow A/D line has been confirmed with major resistance now in the $166.60 to $169.40 area.

The key resistance for the iShares Russell 2000 (IWM) is just above $103. When it is overcome the IWM should then rally to the $104.50-$107 area.

What to do? The stock market needs further strength this week to confirm that the recent lows was a good buying opportunity. This is my favored scenario and recommended long positions in select sectors like emerging markets, materials and utilities should continue to do well.

For those who decided during the market's plunge in January that they had too large a percentage of their portfolio in stocks the rally is an opportunity to adjust your portfolio. In commission free retirement accounts I would suggest you gradually reduce your exposure as the market moves higher. This will allow you to reduce your commitment to stocks enough to reduce your fear level.

My analysis still suggests that the recent drop was a bull market correction not the first phase of a bear market. Therefore I think stocks will post solid yearly gains in 2016 but the action of the economy in the next few months will be important. Of course the technical strength of the current rally will provide clear evidence whether this view is right or wrong and it is important to keep an open mind.

For market commentary during the week please follow me on Twitter where I post commentary daily.