It was another strong week for the stock market even though there was little US economic data the positive momentum from the past three weeks pushed stocks even higher. The further easing by the European Central Bank on Thursday was initially discounted as the Dax surged to new rally highs but then closed on the lows as it had a 500 point range. By Friday morning the bullish argument had won out as the Dax again moved sharply higher.

The comments from the International Energy Agency (IEA) that crude oil prices may have “bottomed out” gave the market a further boost early Friday. Now while this is clearly a short term positive it should be pointed out that they do not have a great record in forecasting oil prices. In 2014 they were looking for crude to be over $100 per barrel the next year.. Of course in 2015 crude never made it over $63 per barrel and closed the year at $38.

The sentiment certainly has seen a major shift in the past month which may be due in part to the firming oil prices which has lessened the fears of a credit default crisis in the energy companies. According to AAII the bullish % rose 5.4% to 37.4% in the last week, up from 19.4% just five weeks ago. The bearish% is now at 24.4% just about half of where it was five weeks ago. I think the bullish% could move to the 45-50% and it is now just barely below the long term average of 38.6%.

Many are now wondering whether the rally from the February lows (The Week Ahead: Is There Blood In The Streets Yet? ) is just a bear market rally that will soon lead to another wave of selling or whether the market has resumed its major uptrend.

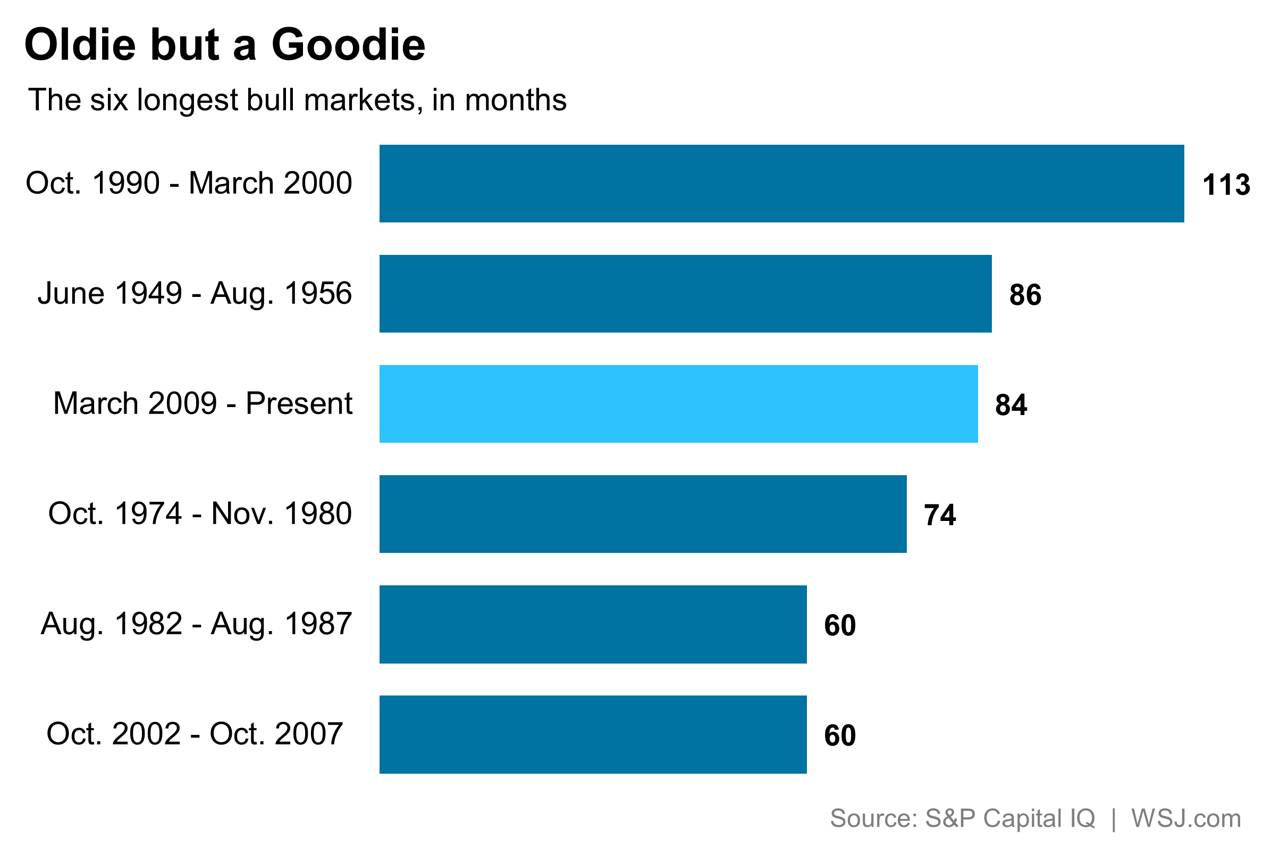

Many who feel we are in a bear market point to how long the current bull market has lasted. This table from the WSJ reveals that our bull market is currently the third longest at eighty-four weeks as the bull market from 1949 to 1956 lasted eight-six weeks. The 1990 to 2000 bull market is still by far the longest. Of course many have been making this argument for a few years and will be right at some point .

One of the other primary arguments is that the US stock market is overvalued. From a recent article "Is the S&P 500 Overvalued" "The S&P 500's current P/E is 21.5 and its Shiller P/E or CAPE (cyclically adjusted P/E) is 24.66. Both numbers are well above their respective historical averages and widely cited, in particular the Shiller PE, as proof the S&P 500 is overvalued. Even the forward-looking forward P/E of the S&P 500 is above average. It's currently 15.7 versus a 10-year average of 14.2. "

Of course I look at the market technically and the last major bear market rally occurred in March 2008 as the NYSE Composite dropped back to the January lows before it turned higher. The NYSE A/D line did make new lows in March, line b, before it began to rally. The five month downtrend (line a) was broken on April 18th. This confirmed a new uptrend in the A/D line, line c.

Once a rally was underway the key resistance was the 61.8% Fibonacci retracement resistance at 9602.33. On May 19th the NYSE had a high of 9687 but then closed at 9602.80. It dropped over the next two days to close over 2% below the 5/19 closing level. The NYSE Composite closed the week below the prior week's low and this reversal was a sign of weakness. After a brief bounce the A/D line turned lower decisively breaking its uptrend, line c, which confirmed that the rally was over.

The AAII bullish% dropped to a low of 19.6% on January 10th 2008 and then had a secondary low of 20.4% on March 13th. In early May the bullish sentiment recorded two consecutive readings of over 50% with readings of 53.2% and 52.8% on May 1st and May 8th. The bearish % hit its low of 22.5% on May 8th. Just six weeks later the bearish% was again well over 50%.

The NYSE Composite closed last week above the 50% retracement resistance at 10,087 that is calculated from the May 21, 2015 high of 11,255. The downtrend from the June-November highs, line a, is at 10,150-200 while the 61.8% resistance is at 10,362. Two consecutive daily closes above this level would clearly be a positive for the intermediate term trend.

Clearly the chart shows strong resistance in the 10,500-10,700 area. The short term downtrend in the NYSE A/D line (line d) was broken in February confirming the new uptrend. The NYSE has rallied 5.7% since then. The longer term downtrend in A/D, line c, was broken last week as it accelerated to the upside overcoming the November-December highs. The A/D line is well above its rising WMA but the width of the gap indicates the market is now overextended .

The weekly chart and technical studies (see Market Wrap) do favor a change in the intermediate term trend. After a market pullback we should see another push to new rally highs. As I have been discussing over the past few weeks the technical damage from the severe January drop means that the market will need some time before it can challenge the 2015 highs.

It is still my opinion that the bull market has resumed and that this is not just a bear market rally. I see no signs of an imminent recession but it will be important that the economic data improves in the coming few months. It would take a sharp weekly downside reversal in the next few weeks and an extended decline in order to alter this outlook.

Sector Outlook

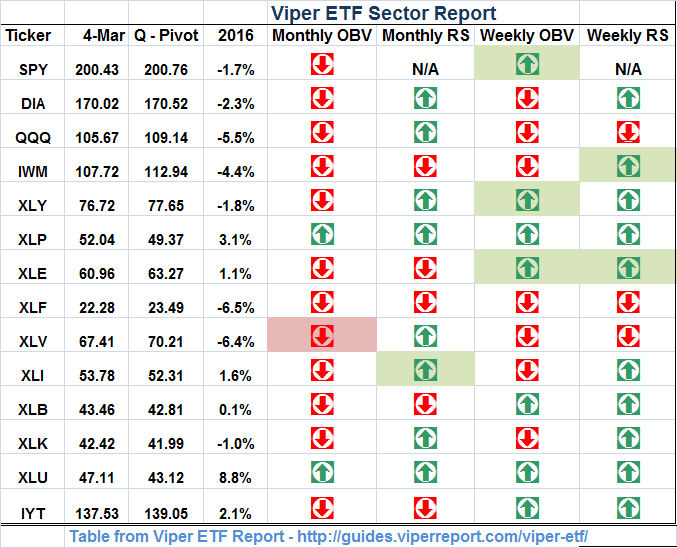

One of the concerns I have about the market is based on my sector analysis as not all sectors have performed equally since the February lows. My weekly scan, that is sent out each Monday to Viper ETF subscribers, shows that only two sectors, the Utilities Sector Select (XLU) and the Consumer Staples Sector Select (XLP) are positive based on the monthly as well as the weekly RS and OBV analysis.

The shading on the chart reveals the changes from the previous period as the weekly OBV on the Consumer Discretionary Sector Select (XLY) turned positive with the close on March 4th. Both the weekly RS and OBV has also turned positive on the Energy Sector Select (XLE).

It is also important to note that the monthly OBV on the Health Care Sector Select (XLV) turned negative in February. The weekly studies will improve this week but are unlikely to turn positive. The monthly OBV on the Industrial Sector Select (XLI) did turn positive last month.

If the market continues to move higher the XLV may reverse to positive as it has been one of the best moneymakers over the past four years. In hindsight I should have jumped on the energy sector last week but was not convinced that a major low had been completed. Subscribers are still holding longs in the XLP, XLU, XLB, DIA, and XHB but have started to take profits on strength as the overall market risk is betting higher.

The Economy

The focus this week will be on the Bank of Japan which starts to meet on Monday and the FOMC meeting that begins on Tuesday. The FOMC has their announcement on Wednesday afternoon.

The PPI is out on Tuesday along with Retail Sales, the Empire State Manufacturing Survey, Business Inventories and the Housing Market Index. Then on Wednesday we have the Consumer Price Index, Housing Starts and Industrial Production.

On Thursday we get the important Leading Economic Indicators (LEI) and the Philadelphia Fed Business Survey , followed on Friday by quadruple witching and Consumer Sentiment.

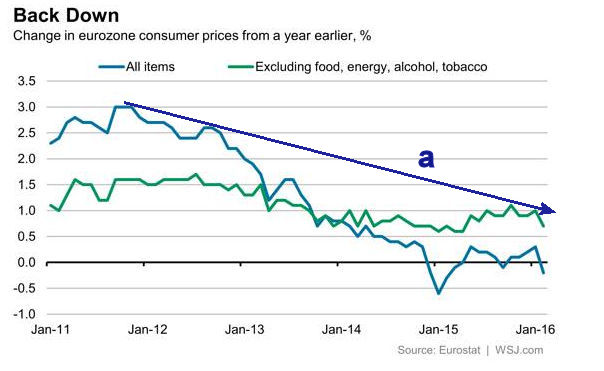

Though there are signs that inflation may be picking up in the US there world economies are more worried about deflation. Consumer prices in the Euro zone are still in a well established downtrend and will take some time before they could bottom out. The specter of deflation helps to justify the ECB's aggressive easing action last week.

Interest Rates & Commodities

In early February " Is This The Stock Market's Secret Weapon?" I alerted investors to the fact that the dollar index had completed a weekly top formation. After the expected oversold bounce back to resistance at line b, it now looks as though the downtrend has resumed.

A drop below the February low at $95.28 will indicate a decline to the 38.2% Fibonacci support at $92.42 while the weekly starc- band is a bit higher at $93.25. There is more important chart and the 50% retracement support in the $90.00 area. The weekly on-balance-volume (OBV) just rallied back to its declining WMA on the recent rally and continues to look weak. There is key OBV resistance at the downtrend line c.

There are now some signs that the Fed is in favor of a weaker dollar and as I noted in February it would have a positive impact on the global economies as well as corporate earnings. The yield on the 10 Year T-Note jumped last week to 1.977% up from the prior week's close at 1.883%. The next major resistance in terms of yield is in the 2.10%-2.20% area.

The weaker US dollar has fueled a further short squeeze in crude oil as according to the latest COT data the short position dropped by 16% in the latest reporting period. Since the data is collected as of Tuesday's close it has likely dropped even further as crude gained $2.58 per barrel last week. There is next chart and retracement resistance in the $40 area and I continue to believe that a 1-2 week pullback is needed before a bottom will be completed.

The Comex gold futures closed the week lower and formed a doji so a close this week below 1238 will trigger a sell signal. A drop to the $1190-$1200 area would not be surprising and should reduce the too high bullish sentiment. Such a correction would likely create a good buying opportunity.

Market Wrap

It was another week of solid gains with the Dow Utilities leading the way up 2.2% followed by a 1.2% gain in the Dow Industrials and 1.1% for the S&P 500. The small caps and Transports lagged last week as they were up just over 0.5%. Once again the market internals were strong as 2087 stocks advanced and just 1104 declined.

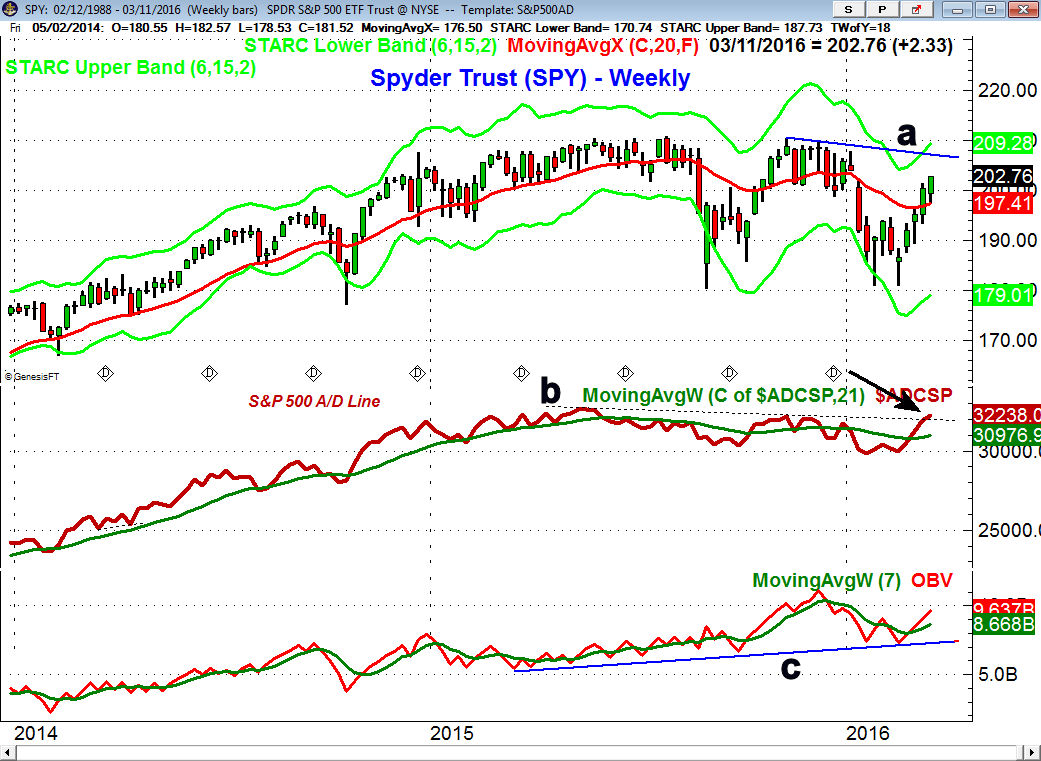

The Spyder Trust (SPY) after exceeded the 61.8% Fibonacci retracement resistance a week ago and settled Friday well above the 200 day moving average at $200.74. The daily starc+ band is at $205.57 with chart resistance from the November-December high, line a, at $207.50. There is initial support now at $197.38 which was last week's low with the rising 20 day EMA at $196.68. The daily starc- band is at $194.80.

The weekly S&P 500 A/D line has closed for the second week above the resistance (line b) from the all time highs. This is a bullish sign for the intermediate term trend and is consistent with an important bottom at the February lows. The A/D line is well above its rising WMA and a pullback to the WMA should create a good buying opportunity.

The weekly OBV has been above its WMA since late February and its WMA is now clearly rising. The daily OBV has started to rise more sharply and is now challenging the December highs as it is trying to catch up with prices.

Many of the beaten down technology stocks have had impressive rallies since the end of January. Last week I took a technical look at some of these stocks (Charting Barron’s Beaten Down Tech Stocks) to see which looked the best technically.

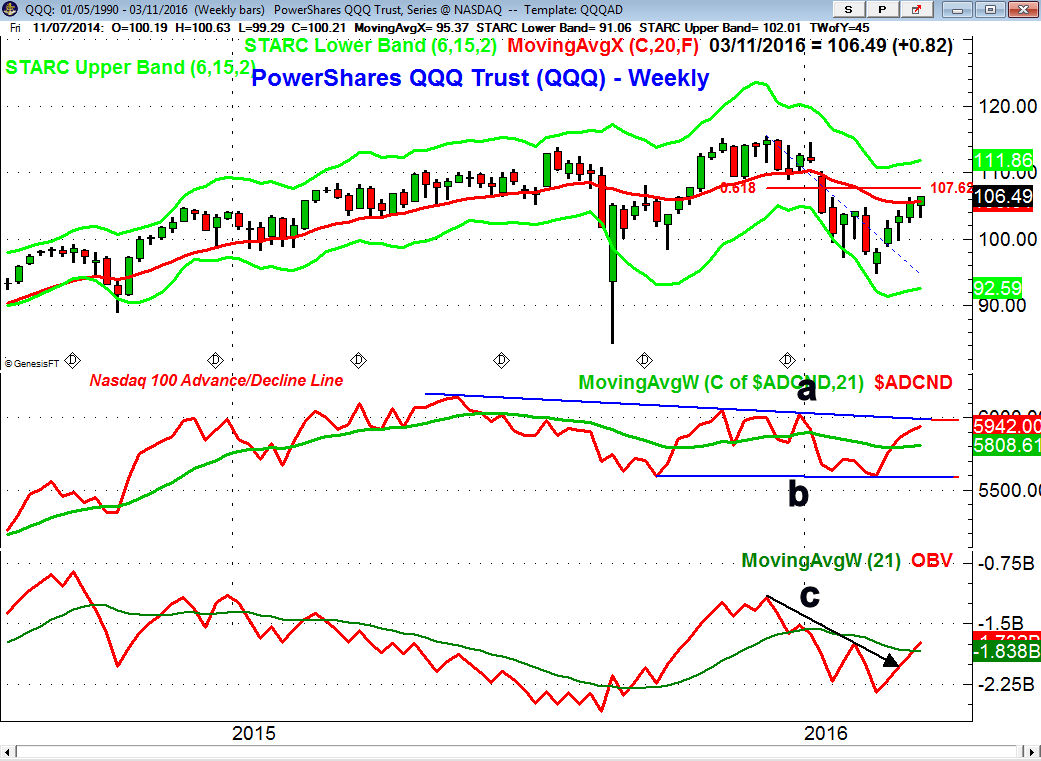

All are part of the PowerShares QQQ Trust (QQQ) which I screen weekly along with the IBD 50 for new Viper Hot Stock trading opportunities . The QQQ is up over 12% from the February lows but still below the 61.8% Fibonacci retracement resistance at $107.62. Once this level is overcome the January high is at $109.60 with the weekly starc+ band at $111.86.

For the third consecutive week the Nasdaq 100 A/D line is above its WMA but is still below the major resistance at line a, which is derived from the all time highs. A strong close above the November-December highs would be a bullish sign. The weekly OBV moved through its downtrend a few weeks ago and has now just surpassed its WMA.

The iShares Russell 2000 (IWM) has just made it back to its major 38.2% resistance with the 50% resistance at $110.65. There is initial support at $104.50-$105 and the 20 day EMA with stronger now at $103.

What to do? The close in the SPY above its 200 day moving average has been enough to shift the sentiment but many still think we are just seeing a bear market rally. My analysis suggests the intermediate trend has changed but one needs to keep an open mind to the market action over the next few weeks.

Many were quite skeptical about my comments on February 6th that "I do expect the SPY to be 5-10% above current levels before the end of the first quarter". The rally has easily exceeded these targets and we still have two more weeks left in the quarter.

The FOMC meeting is likely to cause a pickup in volatility as even though I do not expect them to act on rates next week their comments will be fully dissected. If you have some nice profits from the four week rally I would suggests that you take them early in the week and I advised Viper ETF traders to take a 12.8% profit on their remaining longs in XLB on Friday's open. A sharp selloff is real possibility next week as the market is vulnerable with the FOMC announcement.

If you were uncomfortable about your portfolios losses in January you should have recouped a good part of the losses on the rally. Therefore now might be a good time to reduce your exposure as while their are quite a few stocks that can be bought now most ETFs need a correction to create a good buying opportunity.

Editor's Note: If you like Tom's analysis and would like a free copy of his Viper ETF Report with no obligation, email your request to wentworthresearch@gmail.com.